Market performance in 2023 marked a significant change from 2022, with almost every asset class outperforming the prior year. Both stocks and bonds rallied in November and December after a rough stretch from August to October. Through the first three quarters, bonds were down for the year but then posted their best quarter in more than 20 years in the fourth quarter.

U.S. large-cap stocks, led by the Magnificent Seven, outperformed all asset classes last year. Small-cap stocks made a year-end run after the Fed announced that it was probably finished raising rates and anticipating three rate cuts in 2024. Small-cap stocks had been hit hard earlier in the year following the Silicon Valley Bank crisis. Energy stocks finished the year flat after being the only positive sector in 2022, and Chinese equities pulled up the rear, being the only major asset class to finish in the red.

Each year there are defining themes that dominate the markets. In 2020, it was the global pandemic, which in turn caused the supply chain issues of 2021. In 2022, it was all about inflation. Last year, as we wrote often, it was the emergence of artificial intelligence.

Some of these market and economic themes can be positive while others are negative. As one theme gives way to another, it is important to remember not to get distracted by the narratives and to stick with the investment plan.

We cannot predict what theme will dominate the markets in 2024. The presidential election will be a likely candidate, but the markets historically have done a great job ignoring the election concerns that cause many investors to fret.

Key Themes in the Market by Year

Number of mentions in earnings call transcripts of Russell 3000 companies

This will be no ordinary election year. The below chart played out well last year, during the third year of the presidential cycle. With 2023 ending so strong, we would not be surprised to see a pause in equity markets to start the year and continue the trend of a weak first quarter during the fourth year of the presidential cycle, followed by strength the rest of the year.

Q1 of an Election Year Tends To Be Weak

S&P 500 quarterly performance by presidential cycle (1950-2023)

As we recently wrote, we see many reasons to be bullish in 2024:

1. Inflation continues to show signs of moderating to the Fed target of 2%.

2. Interest rates are normalizing. We expect bond yields to decline in line with falling inflation and slower economic growth. This year, we saw the 10-year Treasury span a huge range from as low as 3.25% in April to as high as 5.02% in October.

3. Consumers appear to have plenty of disposable money in their pockets. Consumer spending should grow more slowly as job gains dimmish. However, on aggregate, consumer financial conditions are nowhere near levels before the great financial crisis.

4. Household wealth and liquidity remain robust.

5. The U.S. government has committed more than $1.4 trillion for capital projects. This has the potential to reshape U.S. manufacturing and energy, and boost the semiconductor industry.

6. Economists expect corporate earnings for companies in the S&P 500 to grow by double digits in 2024. Increased earnings could provide a runway for stocks to head higher.

7. Almost $6 trillion of cash remains on the sidelines. Soaring yields in 2023 pulled cash into money market funds and other short-term instruments, such as Treasury bills and CDs. Lower rates in 2024 could force investors to move money into equities and longer-duration bonds to earn a higher rate of return as cash yields fall.

8. Artificial intelligence captured investors’ hearts last year and contributed to the outperformance of stocks led by the Magnificent Seven. AI applications are spawning innovation across many industries, not just in technology companies.

9. Presidential election years have been good for stocks. There is a tendency for investors to worry about elections (which could prove especially true for the upcoming election), but from a market perspective, that worry hasn’t had much of an impact. Going back to 1952, the stock market has declined just three times in a presidential election year. In re-election years, the S&P 500 has not declined since 1948.

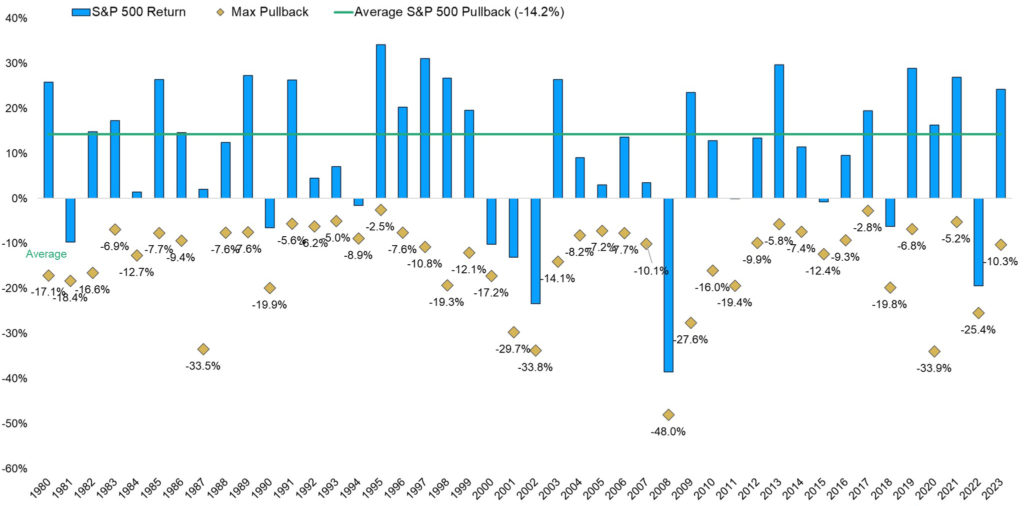

We expect market volatility to rise and cause worry at some time during the year. Market pullbacks are normal, and while markets have gone up over time, it is not in a straight line.

It is good to remember that the average peak-to-trough correction per year is 14.2% since 1980 for the S&P 500.

In 2023, stocks had a 10.3% correction, but finished the year up more than 24%. Even strong years have a correction where the market declines by 10% or more, and it is very rare for the market not to have at least a 5% pullback at some point in a year.

Stocks Go Up and Down, and 2024 Won’t Be Any Different

S&P 500 Index max pullback per calendar year

Remember, much of what we read and hear on the news are market predictions for what economists and analysts think is going to happen. It seems like a long time ago, but at the beginning of 2022, the top 15 Wall Street firms predicted on average that the S&P 500 would finish at 4,950 (from a high of 5,330 to a low of 4,400) and the S&P 500 finished 2022 at 3,839 — a far cry from the prediction. The same analysts last year predicted on average that the S&P would finish 2023 at 4,100 (a high of 4,500 to a low of 3,725). The S&P closed 2023 at 4,769, a gain of over 24%.

For 2024, Wall Street economists see the S&P finishing anywhere from as low 3,300 to as high as 5,400. That is a 2,100-point spread!

At the end of the day, these are predictions, and no one knows for sure how this year will play out. What we do know is that over time, markets tend to rise and staying invested is the best strategy.

The CD Wealth Formula

We help our clients reach and maintain financial stability by following a specific plan, catered to each client.

Our focus remains on long-term investing with a strategic allocation while maintaining a tactical approach. Our decisions to make changes are calculated and well thought out, looking at where we see the economy is heading. We are not guessing or market timing. We are anticipating and moving to those areas of strength in the economy — and in the stock market.

We will continue to focus on the fact that what really matters right now is time in the market, not out of the market. That means staying the course and continuing to invest, even when the markets dip, to take advantage of potential market upturns. We continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been.

It is important to focus on the long-term goal, not on one specific data point or indicator. Long-term fundamentals are what matter. In markets and moments like these, it is essential to stick to the financial plan. Investing is about following a disciplined process over time.

Source: Business Insider, Carson, Goldman Sachs, JP Morgan

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. CD Wealth Management and Bluespring Wealth Partners LLC* are affiliates of Kestra IS and Kestra AS. Investor Disclosures: https://bit.ly/KF-Disclosures

*Bluespring Wealth Partners, LLC acquires and supports high quality investment adviser and wealth management companies throughout the United States.

Fidelity Investments and Fidelity Institutional® (together “Fidelity”) is an independent company, unaffiliated with Kestra Financial or CD Wealth Management. Fidelity is a service provider to both. There is no form of legal partnership, agency affiliation, or similar relationship between your financial advisor and Fidelity, nor is such a relationship created or implied by the information herein. Fidelity has not been involved with the preparation of the content supplied by CD Wealth Management and does not guarantee, or assume any responsibility for, its content. Fidelity Investments is a registered service mark of FMR LLC. Fidelity Institutional provides clearing, custody, or other brokerage services through National Financial Services LLC or Fidelity Brokerage Services LLC, Members NYSE, SIPC.