The last few weeks have reminded us how quickly markets can shift. We also are reminded that this isn’t new. History shows the market has always recovered from previous declines.

Just three weeks ago, the S&P 500 was close to correction territory, the NASDAQ and Russell 2000 indexes were both down more than 10%, and oil prices were over $120 per barrel. While oil prices have come down, they remain higher than pre‑conflict levels.

Historically, sharp increases in oil prices have often preceded recessions and, in some cases, contributed to bear markets. Think back to early 2022, when Russia invaded Ukraine: Oil prices surged to almost $130 per barrel as the Fed began raising rates aggressively.

Stocks dropped almost 20% that year but then rallied hard in 2023, as energy markets stabilized and corporate earnings proved more resilient than investors expected.

While the Iran conflict so far has not proven to be as severe as a typical market drawdown, it is a reminder that markets tend to absorb shocks faster than headlines would lead us to believe. Since 1990, markets have averaged gains of roughly 12% in the first year after an oil supply shock — and more than 32% over the following two years later.

Market selloffs from oil shocks have been short-lived

S&P 500 Index returns following geopolitical-related oil supply disruptions, 1990-2024

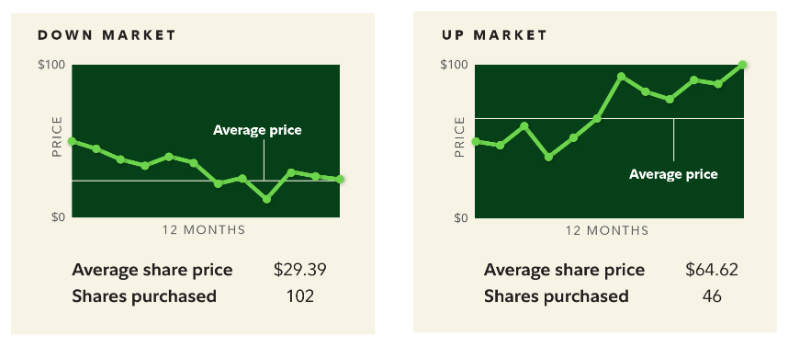

We know how easy it is for investors’ emotions to take over when markets get rough. Dollar-cost averaging is one way to take the emotions out of your investing decisions. With this strategy, you invest money in equal amounts at regular intervals, regardless of which direction the market is going.

By continuing to invest regularly during a volatile or down market, you are more likely to purchase a greater number of shares at lower prices compared to investing during an up market.

Let’s say you invest $250 per month into a stock, index fund or mutual fund. If the stock price is rising, you may be buying a few shares each month, whereas in a down market, you are buying more shares for the same amount of money. On average, investors pay less on per share over time.

Regular investing doesn’t ensure a profit or protect against loss, but if you can buy more shares for the same amount of money for a solid long-term investment, it makes more sense than trying to time the purchase.

Dollar-cost averaging in different markets

Here’s what happens if you invest $250 a month for a year in up and down markets

Emotional reactions to market events are perfectly normal. It is understandable to feel nervous when markets decline, but the actions taken during such periods can determine a successful long-term outcome.

Understanding emotional behaviors such as loss aversion, anchoring, confirmation bias, and availability bias can help you avoid potential mistakes, such as selling at a market bottom.

• Loss aversion is a behavioral bias where investors feel the pain of losses more strongly than the pleasure of equivalent gains. This can show in different ways: refusing to sell something for a loss, selling winners too early, or becoming more conservative after a loss. This also can lead to being risk–averse at the wrong time.

• Anchoring is a bias where one fixates on initial piece of information, such as the purchase price of stock, a target price, or valuation multiple. Once anchored, investors subconsciously compare all future information to that reference point.

• Confirmation bias happens when an investor looks for information to support their belief, while ignoring new information that may contradict that belief. This shows up in overconcentration in favored ideas and the dismissal of contradictory signals.

• Availability bias is a behavioral bias in which investors favor information that is more recent or memorable and give less consideration to information that is less memorable. In simple terms, what comes to mind easily feels more important than it really is. Most often, this results in buying high and selling low, as shown in the illustration below.

Market volatility can be unsettling, but it is not a reason to panic. It can present an opportunity to boost savings and buy more of your investments at lower prices.

If you have a solid plan in place, sticking with that plan — buying more when investments are on sale — can help position you for better outcomes as the uncertain times pass and markets move toward greener pastures.

Understanding behavioral tendencies and how they affect your view of the markets goes a long way to long-term financial success.

The CD Wealth Formula

We help our clients reach and maintain financial stability by following a specific plan, catered to each client.

Our focus remains on long-term investing with a strategic allocation while maintaining a tactical approach. Our decisions to make changes are calculated and well thought out, looking at where we see the economy heading. We are anticipating and moving to those areas of strength in the economy and in the stock market.

We will continue to focus on the fact that what really matters right now is time in the market, not out of the market. That means staying the course and continuing to invest, even when the markets dip, to take advantage of potential market upturns. We continue to adhere to the proven disciplines of diversification, periodic rebalancing, and forward-looking strategies, while avoiding reliance on stale retrospective data.

It is important to focus on the long-term goal, not on one specific data point or indicator. Long-term fundamentals are what matter. In markets and moments like these, it is essential to stick to the financial plan. Investing is about following a disciplined process over time.

Sources: Fidelity, Capital Group