Events in Iran are unfolding quickly, prompting global concern from both a humanitarian standpoint and a market and economic perspective. The war in Iran has sent oil prices surging and U.S. Treasury yields higher.

European and Asian stocks are weaker amid concerns that the conflict could spread to other countries in the Middle East and beyond. There are more questions than answers right now. Historically, events like this have been relatively short-lived from a stock market perspective and have largely been forgotten within six months.

It is important to note that markets are not anticipating any specific outcome from the war. Instead, they are pricing in a wider range of risks due to uncertainty about how long the conflict may last and what Iran may look like in a post-war environment.

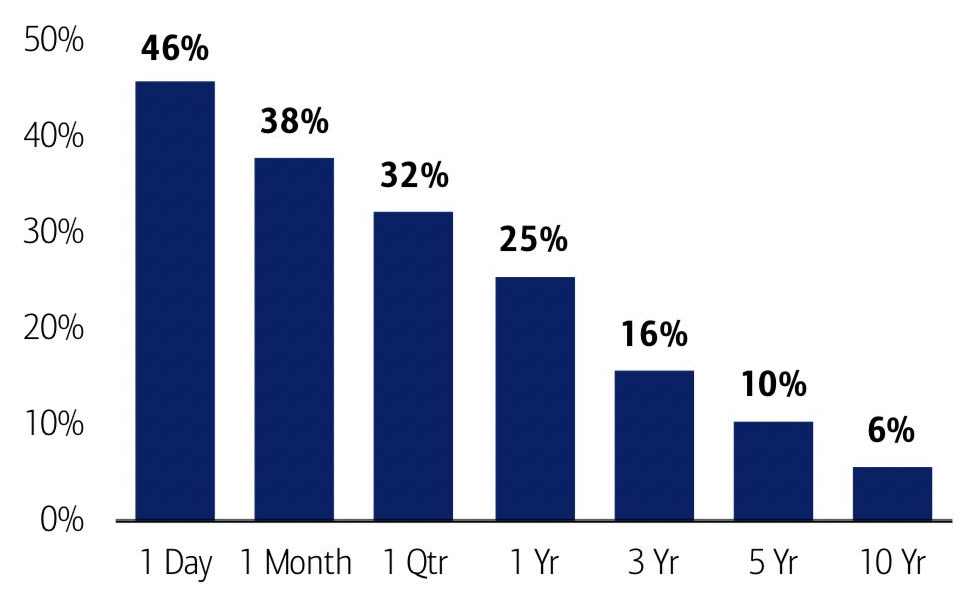

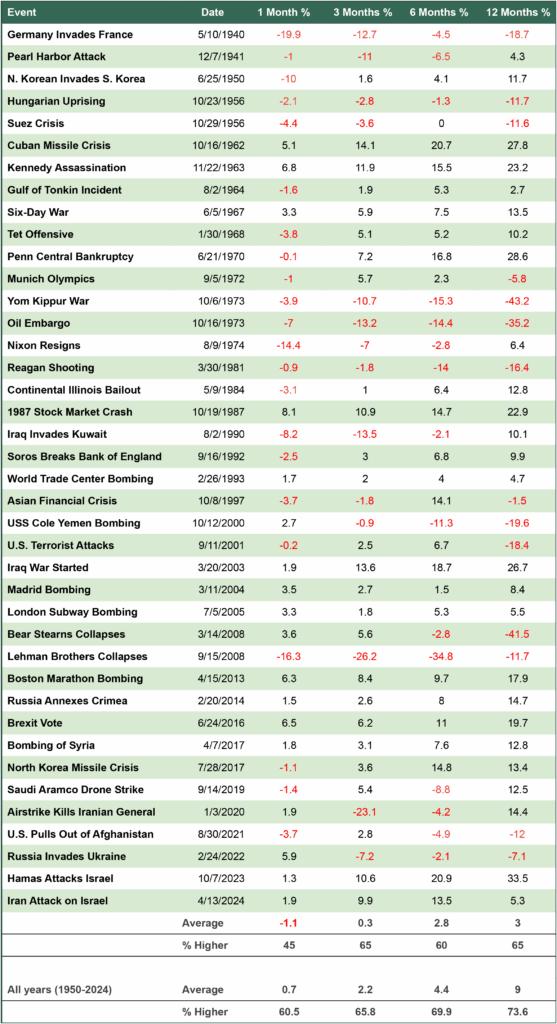

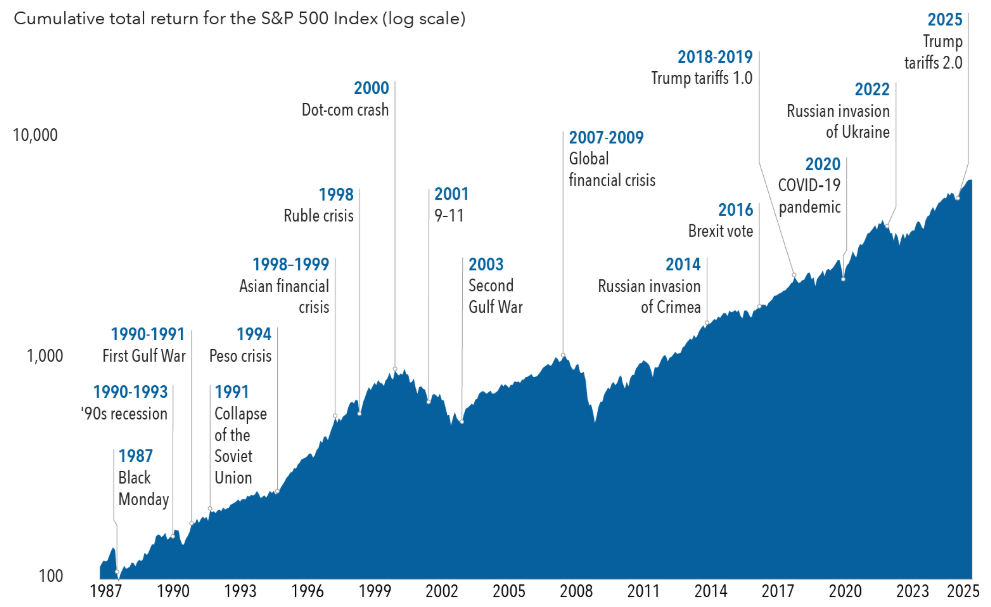

Periods of geopolitical stress often create the sense that the markets are bracing for something bigger. The challenge becomes resisting the urge to make drastic moves in the portfolio.The chart below, which we also shared two weeks ago, shows such events typically do not last long enough or have enough impact to meaningfully change the trajectory of growth.

Over time, investors’ worries erode as emotions give way to market fundamentals, such as corporate profit growth and the pace of the U.S. economy.

How the Market Has Climbed Past Crises

For this conflict in particular, oil is the key economic indicator to watch. Iran exports about 1.5 million barrels of oil per day, and 20% of the world’s oil supply passes through the Strait of Hormuz. If countries become worried about supply constraints, demand could increase, putting further upward pressure on oil prices. The most likely impact from this conflict would be higher oil prices.

However, the U.S. is much less vulnerable to temporary energy spikes because we are now a net exporter of oil, and advances in technology have made it easier to increase domestic production quickly to help offset any declines in foreign production.

At times like this, it is critical not to be swayed by alarming headlines. Sensational predictions rarely come true.

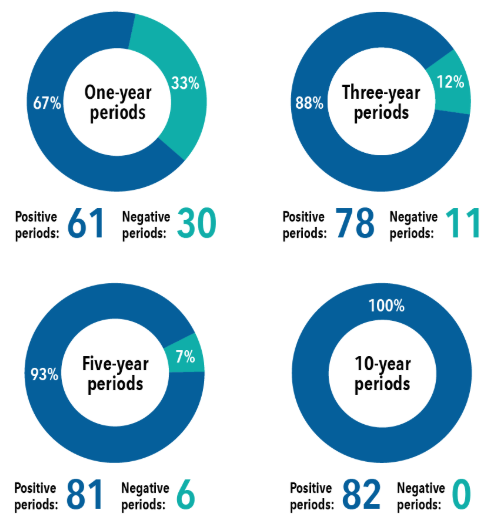

Spending time worrying about events that may happen — or that historically happen rarely — is a great way to scare yourself out of the stock market, which goes up far more often than it goes down.

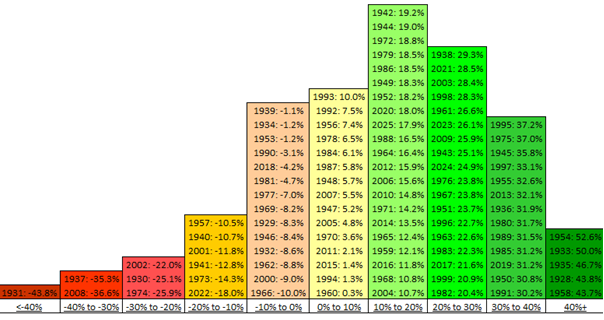

Since 1928, the S&P 500 has finished the year negative 26 times, and in 14 of those years, the decline was less than 10%. In the other 72 years, the market has finished in the positive, meaning that more than 73% of the time, the market ends the year higher.

In other words, nearly three-quarters of the time, people invested in the S&P 500 finished the year ahead.

Distribution of S&P 500 Annual Returns Since 1928

If you are investing for the long run, it’s best to consider your portfolio from a place of optimism or hope, not fear. If you don’t believe things are going to be better in the future than they are today, then the market may not be the place for you.

This doesn’t mean that there won’t be recessions, financial crises, wars, or market crashes in the future, but focusing on the negatives or worrying about the “what ifs” makes it much harder to stay invested for the long run.

We all see the market headlines and emails saying that a market crash is coming, a recession is on the horizon, or today’s market looks like the dot-com bust or the Great Recession. What we’re saying is that major events will happen and markets will fall at times, but most dire forecasts about the future simply don’t come true.

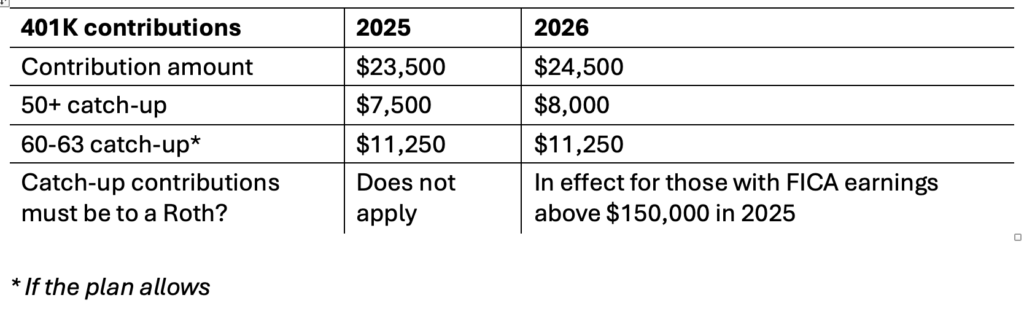

The CD Wealth Formula

We help our clients reach and maintain financial stability by following a specific plan, catered to each client.

Our focus remains on long-term investing with a strategic allocation while maintaining a tactical approach. Our decisions to make changes are calculated and well thought out, looking at where we see the economy heading. We are anticipating and moving to those areas of strength in the economy and in the stock market.

We will continue to focus on the fact that what really matters right now is time in the market, not out of the market. That means staying the course and continuing to invest, even when the markets dip, to take advantage of potential market upturns. We continue to adhere to the proven disciplines of diversification, periodic rebalancing, and forward-looking strategies, while avoiding reliance on stale retrospective data.

It is important to focus on the long-term goal, not on one specific data point or indicator. Long-term fundamentals are what matter. In markets and moments like these, it is essential to stick to the financial plan. Investing is about following a disciplined process over time.

Sources: Capital Group, Fidelity, Carson