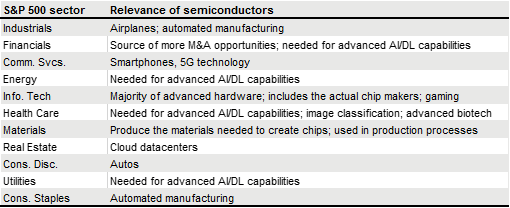

Semiconductors are critical to all sectors of the market, and they’ve been in short supply around the world this year because of pandemic-related factory closures and limited manufacturing, increased demand for electronics and the U.S.-China trade war. Chips aren’t just used for video games; the chart below shows the broad reliance on semiconductors across all industries. Semiconductor chips are in cars, medical devices, smartphones, datacenters, utilities, airplanes and even devices such as toothbrushes and washing machines. Without semiconductor chips, most businesses’ operations would cease to exist.

As companies continue to report second-quarter earnings, a common theme in their reports is very strong semiconductor orders, coupled with low inventories, leading to longer lead times and above-average pricing. As we have written before, this is Supply and Demand 101: Strong demand and low supply lead to higher prices. Businesses look to pass these higher costs to consumers in an effort to protect their profits. However, when raising prices on their input costs, they risk undermining demand for their product, thus lowering profits and prices in the long run.

This gap between supply and demand in semiconductor chips is expected to continue widening. It takes time to add supply; a company cannot just build a new semiconductor manufacturing plant overnight. Manufacturing a chip typically takes more than three months, requiring very clean facilities, large factories — and tens of billions of dollars. Existing chip plants already run 24 hours a day, seven days a week. Manufacturers of semiconductors have expressed confidence in their ability to grow capacity, but any such expansion will be incremental and probably will not close the demand gap for one to two years.

Earnings growth remains robust today, with more than 70% of companies in the S&P 500 having already reported second-quarter earnings. Earnings growth is nearly 85% higher than the prior year. Supply chain disruptions, caused by semiconductor shortages, rising input costs and wages may have an impact on profit margins and slower future earnings growth. Equity markets look forward, anticipating what may happen in the future, and semiconductor supply and demand will have an impact on earnings — and therefore, the market — for the near future.

So, what can we learn from all this? We believe investors should not overreact to market headlines by making sudden and significant changes to portfolios. We continue to closely watch economic data and monitor the COVID variant’s effect on the global economy and Federal Reserve policy, as well as China and its increased regulations and restrictions.

From a portfolio perspective, we continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been. Making market decisions based on what might happen may be detrimental to long-term performance. The key is to stay invested and stick with the financial plan. Markets go up and down over time, and downturns present opportunities to purchase stocks at a lower value.

It all starts with a solid financial plan for the long run that understands the level of risk that is acceptable for each client. Regarding investments, we believe in diversification and in having different asset classes that allow you to stay invested. The best option is to stick with a broadly diversified portfolio that can help you to achieve your own specific financial goals — regardless of market volatility. Long-term fundamentals are what matter.

Sources: JP Morgan, CNBC, Bloomberg

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. Kestra IS and Kestra AS are not affiliated with CD Wealth Management. Investor Disclosures: https://bit.ly/KF-Disclosures