Today is NTX Giving Day in North Texas. It’s an annual tradition through which the Communities Foundation of Texas connects donors with charities in need and fulfills its mission to put giving to work throughout our local communities.

What a great time to think about making charitable donations for both philanthropic and tax purposes! No matter your interests, making gifts to causes you care about can be one of the most meaningful uses of your money. In the end, what really matters is helping an organization that matters to you. The tax benefits from a donation are just icing on the cake.

Along with the intangible rewards that come from helping others, charitable giving may offer a financial benefit for you and your family.

Most donations to charitable organizations come in the form of checks and credit card payments. However, there may be more efficient ways to donate, which in turn help both the charity as well as your pocketbook. Understanding the benefits for different type of donations is important. Here are some options to consider:

• Cash, check or credit card: This is the most simple and straightforward way of donating to charity. It is important to keep a bank record or a receipt from the charity to substantiate a cash gift. Annual income tax deduction limits for gifts to public charities are 30% of adjusted gross income (AGI) for contributions of non-cash assets, if held for more than one year, and 60% of AGI for contributions of cash. If contributions are made in excess of those limits, the excess may be carried over for up to five years. If you do not have appreciated assets to give or want to give cash, it may be beneficial to combine or “bunch” two years’ worth of charitable contributions into one year so you can take advantage of itemizing deductions.

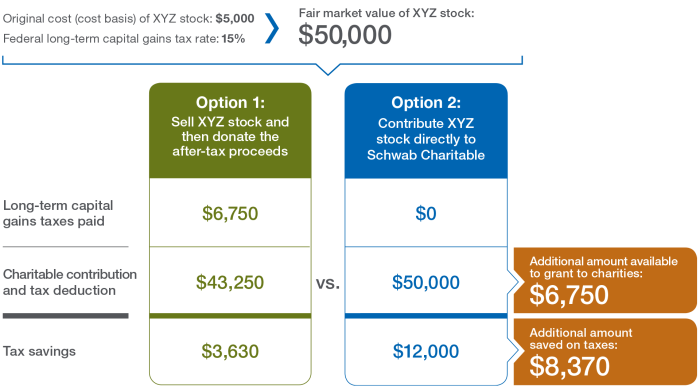

• Appreciated stock: If you donate stock that you have held for at least 12 months, you can deduct the full value of the investment without having to pay capital gains on the appreciation. The current fair market value of the stock is deducted from your taxable income. Often, clients may donate the stock with the biggest winnings, which maximizes savings on capital gains, and then buy back the same stock with cash, which in turn, raises the cost basis. As the chart below shows, if you were to sell appreciated stock and then donate cash to charity (compared to gifting appreciated stock), not only would you save on taxes (the charity does not pay capital gains tax), but the charity would also receive additional monies!

• IRA Qualified Charitable Distributions (QCD): This is an option only for donors over the age of 70 1/2. QCDs allow individuals to donate up to $100,000 annually directly from their IRA to charitable organizations. This reduces the value of the IRA, and the QCD does not count towards the donor’s taxable income. It also counts toward the annual required minimum distribution.

• Donor Advised Fund (DAF): Picture a donor advised fund as your family foundation, without the headache and administrative hassle of setting up a family foundation. A DAF is a charitable account established at a public charity or community foundation that allows donors to recommend grants over time. The donor decides the timing of the donation, the charity that will receive the donation and the amount of the charitable donation made from the DAF. The donor claims the tax deduction upon funding of the DAF. There is not a requirement that the DAF distribute 5% of the fund each year, which may allow the DAF to grow, expanding the available dollars to donate to charities.

At CD Wealth Management, charitable giving is a significant part of our company’s culture. We believe in giving back with our time as well as our pocketbook. We support many causes in the Dallas-Fort Worth area, and we encourage team members to be involved in the community. Each year, during the holiday season, the company makes a charitable donation in each one of our team members’ names to their charity of choice, offering an additional thanks and helping a great cause at the same time.

Please do not hesitate to reach out to us to discuss your charitable options to help you determine the best way to give for your situation. If you are interested in taking part in NTX Giving Day, click here. (Please note that all funding options described above may not be available for NTX Giving Day.)

The CD Wealth Formula

We help our clients reach and maintain financial stability by following a specific plan, catered to each client.

Our focus remains on long-term investing with a strategic allocation while maintaining a tactical approach. Our decisions to make changes are calculated and well thought out, looking at where we see the economy is heading. We are not guessing or market timing. We are anticipating and moving to those areas of strength in the economy — and in the stock market.

We will continue to focus on the fact that what really matters right now is time in the market, not out of the market. That means staying the course and continuing to invest, even when the markets dip, to take advantage of potential market upturns. We continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been.

It is important to focus on the long-term goal, not on one specific data point or indicator. Long-term fundamentals are what matter. In markets and moments like these, it is essential to stick to the financial plan. Investing is about following a disciplined process over time.

Sources: Baird, BMO, Schwab

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. CD Wealth Management and Bluespring Wealth Partners LLC* are affiliates of Kestra IS and Kestra AS. Investor Disclosures: https://bit.ly/KF-Disclosures

*Bluespring Wealth Partners, LLC acquires and supports high quality investment adviser and wealth management companies throughout the United States.