We are now in the dog days of summer, and the first half of 2026 is behind us. It has been a remarkable six months for investors. Markets navigated the continued AI boom, conflict in the Middle East, and a sharp first-quarter correction before staging a powerful rally that pushed major indices to new all-time highs by the end of June.

Markets sold off as investors weighed the escalating conflict between the U.S. and Iran, higher oil prices, and increased geopolitical uncertainty. At one point, the NASDAQ and S&P 500 fell nearly 10% from their highs. As tensions eased, stocks rebounded sharply, led by companies benefiting from the continued growth of artificial intelligence.

Rather than the Magnificent Seven stocks leading the way as they had in recent years, gains were led by companies supplying AI infrastructure, such as semiconductor, memory, and data center businesses. In fact, the Magnificent Seven were down more than 3% during the first half of the year.

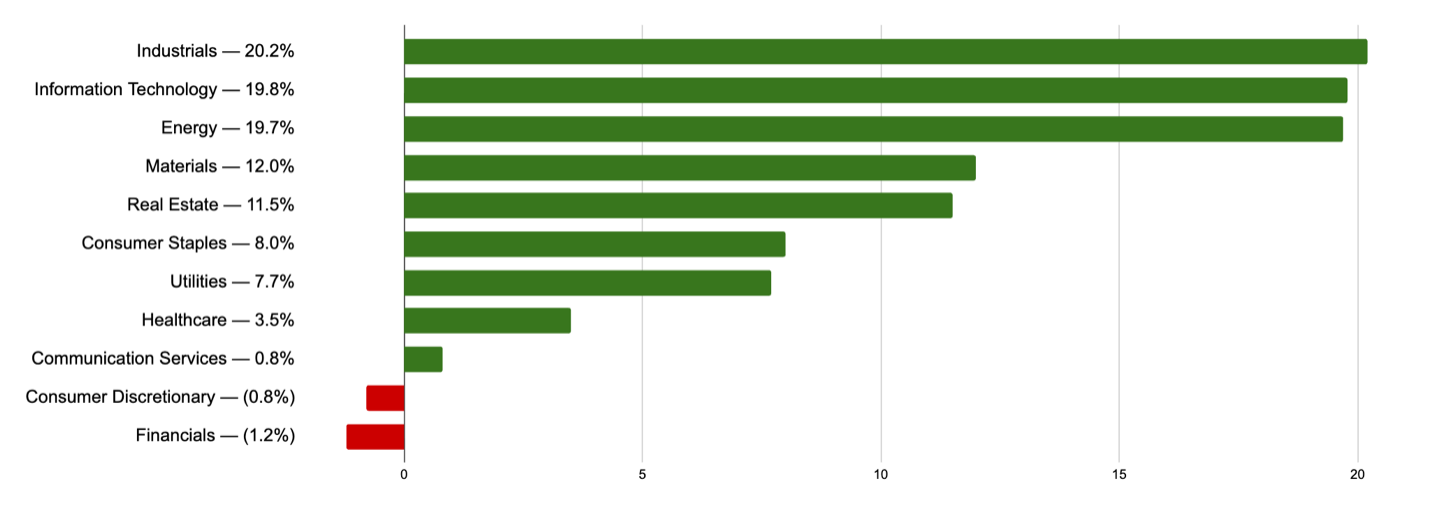

Corporate earnings proved to be the primary reason stocks overcame geopolitical concerns, with double-digit earnings for S&P 500 helping to justify higher valuations. The rally was quite broad-based, with only two of the 11 sectors in the S&P 500 finishing the first half of the year with negative returns. Energy stocks performed similarly to technology stocks due to a jump in oil prices from the Middle East conflict.

S&P 500 Sector Performance

(January-June 2026)

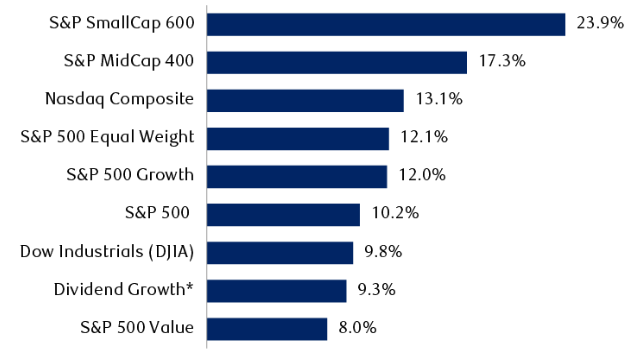

Small-cap stocks, which tend to do well when manufacturing and job-growth trends are strong, led all major indexes with a gain of more than 20% during the first half of the year. Mid-cap stocks also benefited from the AI-driven data center buildout, as well as relatively inexpensive valuations compared to large-cap equities.

International stocks continued to show the strength they demonstrated in 2025, generating similar returns to U.S. stocks during the first half of the year. Emerging markets have been among the best-performing asset classes this year, led by South Korea and Taiwan, as demand has strengthened for semiconductors and other technologies tied to the AI boom.

Strong Returns for Equity Indexes

First-half 2026 total returns of key indexes and styles (includes dividends)

The U.S. economy remained resilient in the first half of the year despite inflation and geopolitical uncertainty. Capital investment remained strong, especially in areas tied to artificial intelligence, while unemployment remained at 4.3%, near historical lows.

Consumers generally proved to be resilient despite higher prices. However, lower-income consumers are feeling the strain, and the divide between the haves and the have-nots is growing wider. Higher-income earners and consumers have benefited from a strong stock market and have been able to spend more on travel and luxury goods, while lower-income earners have not shared in the benefit of rising asset values.

Higher oil prices have pushed up the cost of many goods and contributed to higher prices for transportation and other services. Inflation also led to higher yields for the 10-year and 30-year Treasury bonds, with the 30-year breaching 5% during the first half of the year. At the start of the year, investors widely expected the Federal Reserve to reduce interest rates. Today, expectations have shifted, with many anticipating that the Fed will keep rates higher for longer or even increase rates if inflation continues to move higher.

In May, Kevin Warsh replaced Jerome Powell as chair of the Federal Reserve Bank, adding uncertainty around the future direction of monetary policy. The longer inflation remains higher, the greater the impact on economic growth. Crude prices have fallen significantly from their highs, and gasoline prices have dropped, helping the consumer.

This bodes well for the second half of the year. AI will remain at the forefront of investors’ minds, and we expect some market jitters as the November midterm elections draw near. However, elections have historically been more noise than substance and do not change our long-term outlook for the market.

We do not know if we are in the middle of an AI bubble — and if we are, when it may burst. Bubbles typically last longer than investors expect. The S&P 500 has doubled since the end of 2022, yet only one-fourth of that expansion is due to multiple expansion (valuations), while roughly three-fourths has been driven by earnings growth and dividends. The key remains staying diversified while maintaining exposure to technology stocks and the AI trade.

While uncertainty will undoubtedly remain, our approach does not change. We look forward to helping you stay focused on your long-term goals through the remainder of 2026.

The CD Wealth Formula

We help our clients reach and maintain financial stability by following a specific plan, catered to each client.

Our focus remains on long-term investing with a strategic allocation while maintaining a tactical approach. Our decisions to make changes are calculated and well thought out, looking at where we see the economy heading. We are anticipating and moving to those areas of strength in the economy and in the stock market.

We will continue to focus on the fact that what really matters right now is time in the market, not out of the market. That means staying the course and continuing to invest, even when the markets dip, to take advantage of potential market upturns. We continue to adhere to the proven disciplines of diversification, periodic rebalancing, and forward-looking strategies, while avoiding reliance on stale retrospective data.

It is important to focus on the long-term goal, not on one specific data point or indicator. Long-term fundamentals are what matter. In markets and moments like these, it is essential to stick to the financial plan. Investing is about following a disciplined process over time.

Sources: Carson, CNBC, Fidelity, Kestra Investment Management, RBC