Lately, it feels like every time you tune into a business network, they are talking about the possibility of a private credit crisis. Private credit refers to loans made by non-bank lenders, such as private equity firms like Blackstone, KKR, and Apollo, to name a few. Private credit offers borrowers faster, more customized access to financing than traditional bank lending.

Historically, institutional investors have invested in private credit in search of higher yields — often double digits — and lower correlation to publicly traded stock and bond markets. Over time, private credit has expanded into more portfolios through funds designed for individual investors.

Many private loans do not trade frequently, which can make them less liquid and more difficult to sell quickly when markets turn volatile. Most loan terms are three to seven years, while investors are typically able to ask for redemptions quarterly.

Private credit has moved from a niche corner of the financial system to an established component of the below-investment-grade credit markets. What began in the mid-2000s as a relatively small and specialized form of nonbank lending has grown into a significant source of financing for small and medium‑sized companies, operating alongside the leveraged loan and high‑yield bond markets.

There are many different types of private credit loans, with the most common being direct lending, mezzanine or second-lien debt, distressed debt, special situations and asset-based finance.

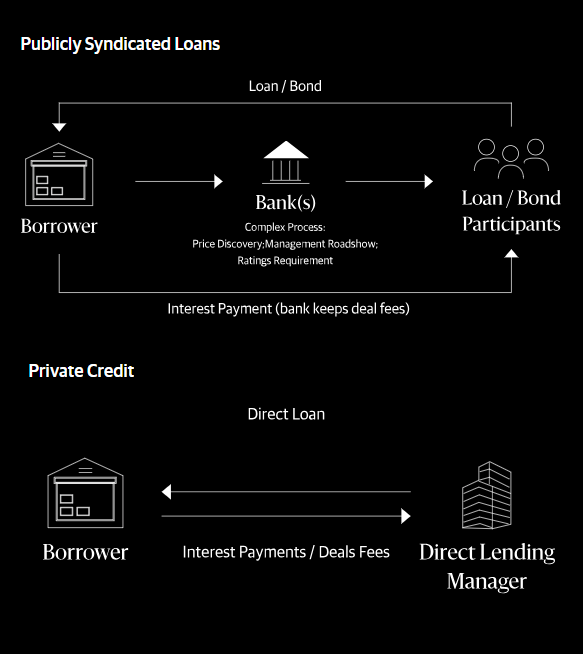

How private credit works

The borrower, which could be a private or public company, negotiates privately with a non-bank lender on the terms of the loan. Private credit often contains a floating rate and is structured with customized terms unique to the borrower and the lender.

Historically, most investors viewed these loans as below investment grade. As private credit has evolved, the types of companies accessing it have expanded as well; borrowers ranging from blue-chip companies to small and mid-size companies may seek funding through private credit markets to support their capital needs.

Why would borrowers turn to private credit?

• Flexibility for borrowers: Private credit allows borrowers and lenders to structure more flexible deals than traditional lending. Borrowers also can get loans and financing faster.

• Bank regulatory changes: Increased regulations and capital requirements make it harder for banks to extend loans.

• Ability to avoid equity financing: Borrowers can access money without diluting ownership.

Putting it in context

Private credit’s growth has been substantial. Over roughly 20 years, private credit assets have increased nearly 20‑fold, reflecting both sustained investor demand for higher-yielding credit assets and changes in bank regulation. Today, private credit features prominently in corporate capital structures and institutional portfolios — as well as an increase in banks’ own lending exposures through financing provided to private credit managers.

Recent events have brought attention to how risk is evolving as the market matures. Private credit is subject to the same underlying economic forces that affect other risky markets, illustrated by restructurings and write‑downs at borrowers such as Tricolor and First Brands, warnings about market stresses in late 2025, and more recent pressure linked to revised assumptions in certain software‑as‑a‑service (SaaS) business models.

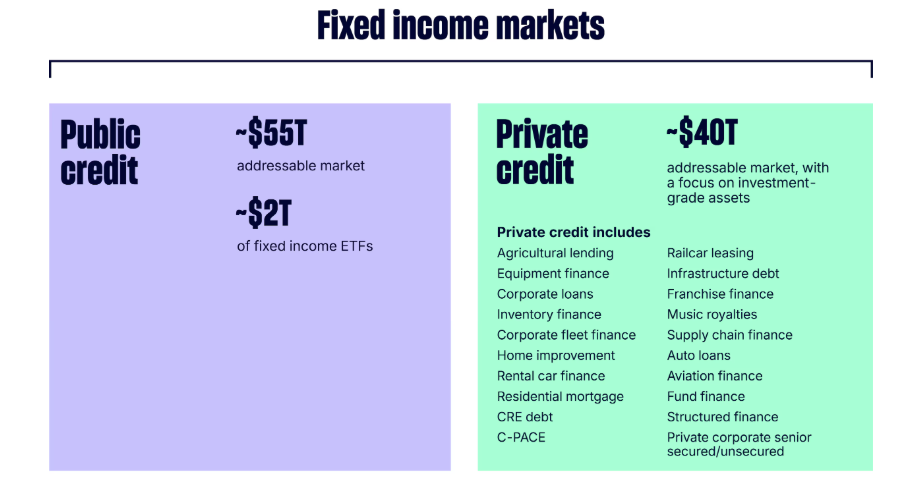

The private credit market, now estimated at approximately $2 trillion to $3 trillion, is experiencing a period of significant stress characterized by high-profile redemption requests and mounting concerns over loan quality. While the asset class grew rapidly after the 2008 financial crisis as banks retreated from certain lending, it is now facing its first full test in an environment of higher interest rates.

One recent area of stress in the private credit market involved a business development company (BDC) called Blue Owl. (BDCs are investment vehicles designed to provide capital to small and mid-sized businesses, often by making private loans.) In Blue Owl’s case, investor withdrawals were limited due to an overwhelming request from investors seeking to access their capital.

Why is the market seeing high redemptions?

1. Redemption squeeze: Major funds are seeing record levels of investors trying to pull their money out, leading to withdrawal caps.

• BlackRock Inc. capped withdrawals from its HPS Corporate Lending Fund at 5% after requests nearly doubled that amount.

• Blackstone Inc. allowed record redemptions of 7.9% from its flagship BCRED fund.

• Cliffwater LLC and Blue Owl Capital have also recently faced significant redemption pressure.

• JPMorgan Chase & Co. has reportedly restricted some lending to private credit funds after marking down the value of certain loans in their portfolios.

2. Rising default rates and asset quality: Signs of borrower distress are becoming more visible across the industry.

• Default rates: The U.S. private credit default rate rose to 5.8% in January, up from 5.6% in December.

• Shadow defaults: The rate of companies requiring unexpected changes to loan terms (often signaling distress) jumped from 2.5% to 6.4% over the past year.

• PIK loans: There is an increasing use of payment-in-kind (PIK) interest, where borrowers defer cash interest by adding it to their principal debt. PIK income reached roughly 8.8% of total investment income in late 2025.

• Free cash flow: Around 40% of private credit borrowers now have negative free cash flow, significantly higher than the 25% seen in 2021.

3. Sector-specific and structural risks

• AI disruption: Concerns are mounting over loans to software firms, whose business models face disruption from rapid advancements in artificial intelligence.

• Opacity and valuations: Skeptics, including JPMorgan CEO Jamie Dimon, have warned of “cockroaches” (hidden problems) due to the market’s lack of transparency and potentially stale asset valuations.

• Concentration: Many direct lending portfolios are heavily weighted toward the software industry, which may constrain future performance.

4. Shifting market opportunities: Despite the current squeeze, some market segments are seeing growth or strategic shifts.

• Asset-based finance (ABF): Investors are increasingly looking at ABF — lending against physical collateral like aircraft or equipment — as a more resilient alternative to corporate direct lending.

• Retail expansion: A 2025 executive order paved the way for retail investors to allocate retirement funds like 401(k)s into private credit, potentially bringing a massive new wave of capital to the sector.

• Opportunistic funds: New “war chests” of approximately $100 billion have been raised by distressed and opportunistic credit funds to snap up assets if the market continues to slide.

5. Liquidity mismatch: Investors are pulling funds from private credit lenders, but private loans are illiquid. Funds offering quarterly liquidity may limit withdrawals to keep from having to sell off loans at low values to meet redemption requests.

6. Valuation and transparency risk: Unlike publicly traded stocks and bonds, private loans do not trade on exchanges. Their value is determined by the fund manager or third-party valuation firms. This can lead to pricing that doesn’t reflect real-time market declines. In a crisis, the lack of a clear market price can make it difficult for an investor to know the true worth of their holding.

Comparisons to 2008

Some observers have started drawing parallels between the private credit market today and the conditions that preceded the 2008 financial crisis, including the lack of transparency within private credit funds and asset managers halting withdrawals. Additionally, private credit lenders have made substantial loans to the tech sector —particularly software companies — though we don’t know the full extent because of a lack of transparency.

Falling asset prices can be an early warning signal, but markets aren’t always rational. The private credit market makes up less than half of the mortgage universe in 2008, which is a positive. Default rates remain low, though they are rising.

Investing in private credit involves risk, and those risks have intensified as the market has grown. While private credit may offer higher yields due to illiquidity premiums, the lack of transparency and liquidity outweigh the potential income, in our opinion.

At CD Wealth, being able to access funds when needed remains the utmost priority. At this moment, many investors in private credit cannot access their funds and the true value of the portfolio remains unknown. We will continue to closely monitor private credit and its potential impact on the rest of the market.

The CD Wealth Formula

We help our clients reach and maintain financial stability by following a specific plan, catered to each client.

Our focus remains on long-term investing with a strategic allocation while maintaining a tactical approach. Our decisions to make changes are calculated and well thought out, looking at where we see the economy heading. We are anticipating and moving to those areas of strength in the economy and in the stock market.

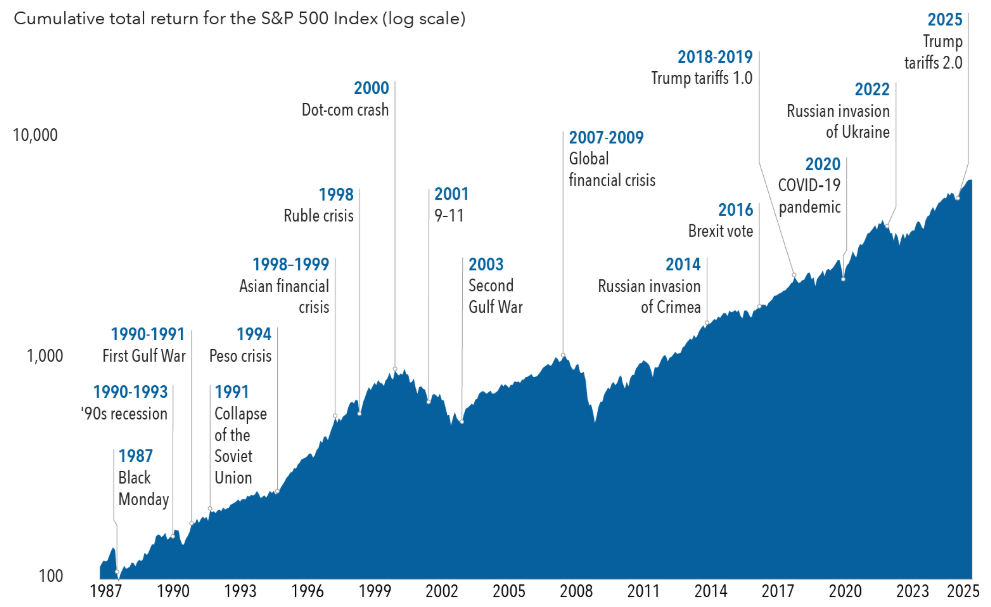

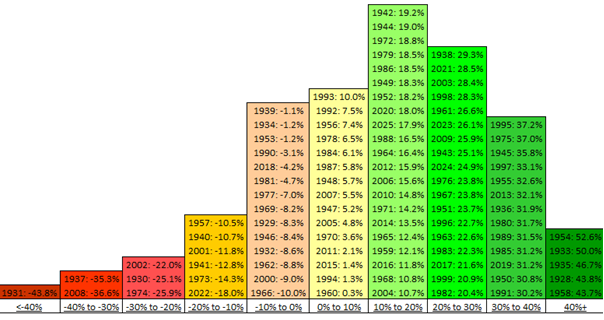

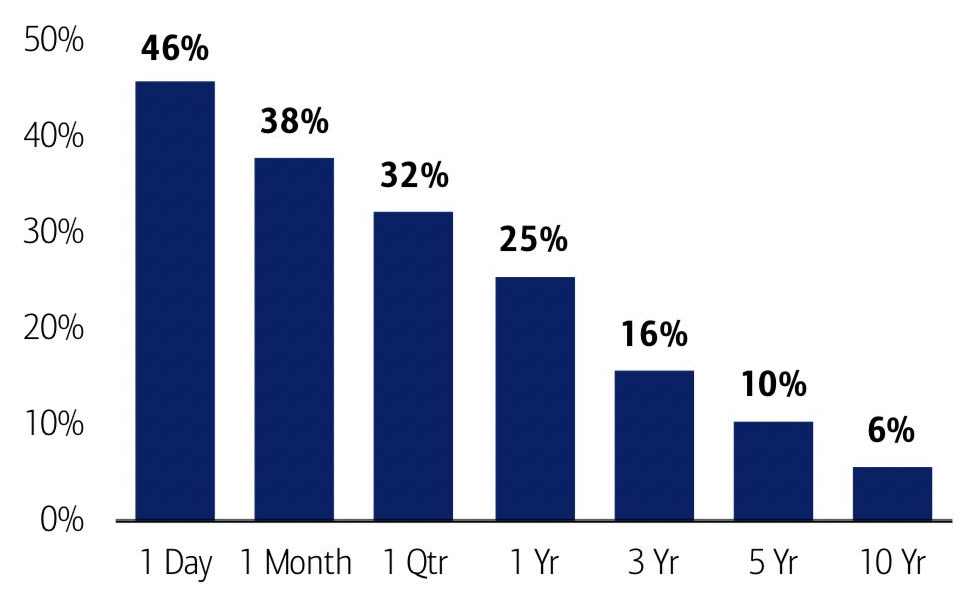

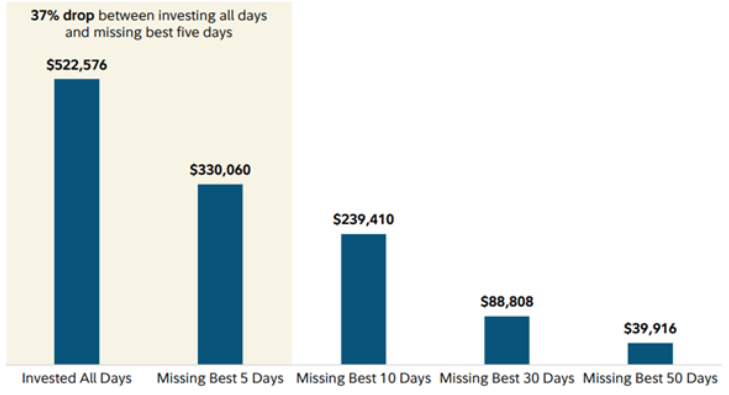

We will continue to focus on the fact that what really matters right now is time in the market, not out of the market. That means staying the course and continuing to invest, even when the markets dip, to take advantage of potential market upturns. We continue to adhere to the proven disciplines of diversification, periodic rebalancing, and forward-looking strategies, while avoiding reliance on stale retrospective data.

It is important to focus on the long-term goal, not on one specific data point or indicator. Long-term fundamentals are what matter. In markets and moments like these, it is essential to stick to the financial plan. Investing is about following a disciplined process over time.

Sources: State Street, US Bank, Bloomberg, Barrons, CNBC