With so many factors causing markets to move, we’re always on the lookout for the biggest stories, the ones that will affect our economic outlook. This week’s headlines cover Big Tech, the race to a COVID vaccine and even the return of disinfectant wipes.

+++

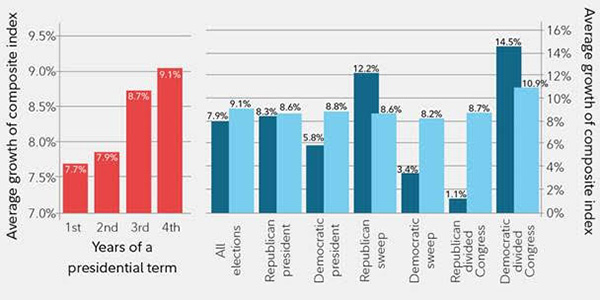

From Forbes: With fewer than 100 days left until the election, some investors are worried about the economic pros and cons of either candidate, but at least one expert believes Wall Street’s fixation on politics is misplaced.

TL;DR: There may be a relationship between the actions of a president and the performance of the market, but in general, the economy may have more to do with business cycles than the occupant of the White House. No matter who’s in office, investors can take comfort that in the long run, “buy and hold” worked best.

+++

From The New York Times (subscription required): Congressional hearings for the heads of Amazon, Apple, Facebook and Google promise to be a spectacle. Whether it’s more theater than substance, some say the hearings show momentum toward regulations.

TL;DR: “The C.E.O.s don’t want to be testifying. Even having this collective hearing creates a sense of quasi-guilt just because of who else has gotten called in like this — Big Pharma, Big Tobacco, Big Banks,” said Paul Gallant, a tech policy analyst at the investment firm Cowen. “That’s not a crowd they want to be associated with.”

+++

From The Wall Street Journal (subscription required): Two of the most advanced experimental coronavirus vaccines entered the pivotal phase of their studies this week, with the first subjects receiving doses of vaccines developed by Moderna and Pfizer.

TL;DR: Researchers plan to enroll 30,000 people in separate last-stage — or phase 3 — trials, the results of which will determine whether the vaccines protect against symptomatic COVID-19 and whether they should be cleared for widespread use.

Related: Think twice before speculating on a COVID-19 cure (CD Wealth Management)

+++

From CNBC: While toilet paper has mostly returned to the shelves since the panic buying of the early pandemic days in March, disinfectant wipes are still in short supply, thanks to supply chain disruptions due to competition with PPE manufacturers for the same raw materials.

TL;DR: The return of disinfectant wipes and cleaning supplies may lag behind demand well into 2021, even with companies ramping up production efforts. Manufacturers predict demand will last even beyond introduction of a COVID vaccine because of long-term shifts in consumer behavior.

+++

From NPR: It should come as no surprise that gold prices started going up as coronavirus started to spread; in uncertain times, investors tend to put their money in gold because it’s considered a “safe haven” for investors worried over instable financial markets.

TL;DR: Even though high gold prices traditionally indicate uncertainty, financial markets have generally been performing well, thanks to aggressive steps taken by the Fed. But many experts caution that market instability could be likely to continue until there is a COVID-19 vaccine, and there also are market experts who suggest that gold prices could continue to climb in the meantime.

______

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. Kestra IS and Kestra AS are not affiliated with CD Wealth Management.