As 2021 comes to an end, the time has come to review some year-end strategies to ensure that your wealth plan reflects any changes in your circumstances or your goals, the economic landscape and current tax environment. We recommend that you review the following checklist for planning strategies to consider; some may apply to you, while others may not. We recommend speaking with your CPA or accountant to review as well.

Income tax strategies

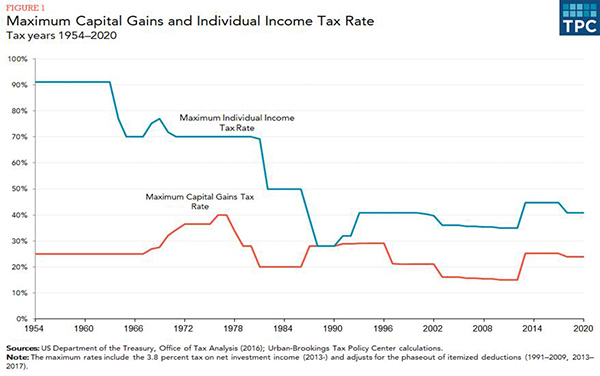

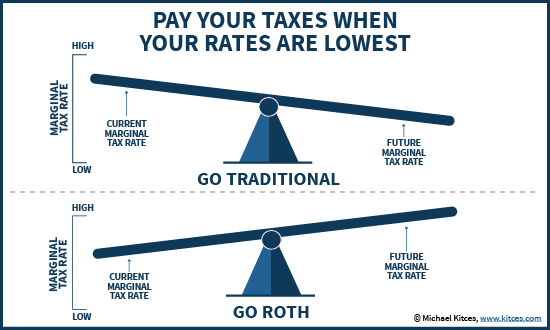

• Traditional year-end planning focuses on deferring income to a future year and accelerating deductions into the current year. However, if you anticipate that your marginal income tax rates will increase next year — whether due to increased income or changes in tax legislation — you may consider accelerating income into 2021 and deferring deductions to 2022.

• If you anticipate being in a lower taxable income bracket in 2022:

— Defer income and any sale of capital gain property (if possible) to postpone taxable income.

— If you are itemizing on your tax return, bunch your medical expenses in the current year to meet the percentage of your adjusted gross income needed to claim those deductions.

— Make your January mortgage payment in December so that you can deduct the interest on your 2021 tax return.

Tax-related investment strategies

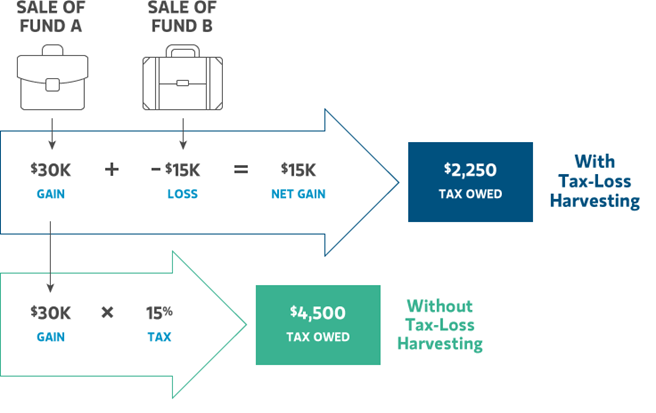

• Tax-loss harvesting is the strategy of selling securities at a loss to offset a capital gain tax liability. It involves selling a taxable investment that has declined in value, replacing it with a similar investment and using the loss incurred to offset any gains.

— Short-term losses are best used to offset short-term gains, and long-term losses can be used to offset long-term gains. Losses can help offset $3,000 of income on a joint tax return in one year.

— Be aware that the IRS wash-sale rule dictates that you must wait at least 31 days before buying back a holding that is sold for a loss.

• Make sure you have satisfied your required minimum distribution (RMD). Once you turn 72 years old, you are required to take minimum distributions from your traditional IRAs and most employer-sponsored retirement plans.

— RMDs were not required in 2020 after Congress passed the CARES Act in response to the pandemic, but minimum distributions resumed in 2021, and failure to take them may result in a 50% penalty.

— You may have an RMD for an inherited IRA, depending on when you inherited it. (Tax laws have changed for newly inherited IRAs.)

Retirement planning strategies

• Maximize your IRA contributions. You may be able to deduct annual contributions of up to $6,000 to your traditional IRA and $6,000 to your spouse’s IRA ($7,000 if over age 50).

• Make a Roth contribution if you qualify under the applicable income limits.

• Consider increasing or maximizing your 401(k) contribution. For 2021, the maximum is $19,500 for those who are younger than 50 and $26,000 for those who are 50 or older.

• Consider contributing to a Roth 401(k) plan if your plan allows.

• Consider setting up a Roth IRA for each of your children who have earned income during the year.

• Determine the optimal time to begin taking Social Security benefits if you over age 62.

Gifting strategies

• Consider making gifts up to $15,000 per person as allowed under the federal annual gift tax exclusion. In 2022, the gift tax exclusion is projected to increase to $16,000 per person.

• Take advantage of the ability to deduct up to 100% of adjusted gross income (AGI) for a cash gift to a public charity in 2021.

• Create a donor advised fund for an immediate income tax deduction and provide immediate and future benefits to a charity over time.

• If you already have a donor advised fund, consider gifting appreciated assets that have been held longer than one year to get the fair market value income tax deduction while avoiding income tax on the appreciation.

• Combine multiple years of charitable giving into a single year to exceed the standard deduction threshold.

• If you are over age 70 ½ (or 72, depending on your date of birth), consider making a direct transfer from an IRA to a public charity. The distribution is excludable from gross income.

Wrapping up 2021, planning for 2022

• Work with your CPA to provide capital gains and investment income information for a more accurate year-end projection.

• Check your Health Savings Account contributions for 2021. If you qualify, you can contribute up to $3,600 (individual) or $7,200 (family), plus an additional $1,000 catch-up if you are over 55.

• Discuss major life events with CD Wealth Management to confirm you have clarity in your current situation.

• Double-check your beneficiary designations for employer-sponsored retirement plans, IRAs, Roth IRAs, annuities, life insurance policies, etc.

• Review that you have a trusted contact on each of your accounts to help protect assets against fraud.

So, what can we learn from all this? The end of year is a perfect time to review your financial planning needs. This includes reviewing the investment portfolio, assessing year-end tax planning opportunities, reviewing retirement goals and managing your wealth transfer and legacy plans. The checklist above includes just some of the items that may apply to your family. We are happy to meet to discuss any of the above to ensure that you remain on track with your financial profile.

From a portfolio perspective, we continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been. Making market decisions based on what might happen may be detrimental to long-term performance. The key is to stay invested and stick with the financial plan. Markets go up and down over time, and downturns present opportunities to purchase stocks at a lower value. As we say each week, it is important to stay the course and focus on the long-term goal, not on one specific data point or indicator.

It all starts with a solid financial plan for the long run that understands the level of risk that is acceptable for each client. Regarding investments, we believe in diversification and having different asset classes that allow you to stay invested. The best option is to stick with a broadly diversified portfolio that can help you to achieve your own specific financial goals — regardless of market volatility. Long-term fundamentals are what matter.

Sources: BNY Mellon, Forbes, RBC

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. Kestra IS and Kestra AS are not affiliated with CD Wealth Management. Investor Disclosures: https://bit.ly/KF-Disclosures