Holidays serve as a good reminder to enjoy the time we get to have with our family, especially our parents and older relatives. We are hopeful it also can be a time to have meaningful conversations with loved ones.

For those of us with aging parents, it’s hard to watch them grow older. After all, we are used to them taking care of us, not the other way around. Through the financial planning process, we often work to understand financial considerations for family members and parents, whether that means an inheritance or financial responsibility for loved ones. If you have not had the conversation with your parents, now is the time. The baby boomer generation and their parents come from a time when people typically did not discuss certain “off-limits” topics, but finances, health care and other issues are no longer taboo.

How do I start the conversation with my parents?

Each family situation is unique; the conversations you may need or want to have can look different from other families. It’s not wise to put the conversation off until your loved ones start to experience health declines, because then you will be forced to make decisions on the fly. You should not feel pressured to have the entire conversation in one sitting — break the conversations up into different days or over the course of several months. Also, it is helpful to plan for the conversation. Ask yourself what you hope to accomplish, what concerns you want to discuss and what the ideal outcome is before you begin.

Planning helps reduce the anxiety of having the conversation and sets you and your family up for success. It is helpful to approach the process as a partnership. Use “we” statements so they don’t feel targeted and understand you are in this together for their wellbeing.

Uncomfortable conversations take time, patience and perseverance. Do not take it personally if the conversation doesn’t go the way you envisioned; this is not about you, after all.

Pick a time, space and place where you and your family won’t feel rushed. Consider a neutral location and anticipate interruptions. Minimize distractions if possible by turning off the TV and your phones. Remember to reframe your language to reinforce that this is a partnership and you only want to help.

Don’t make the initial conversation all about the money, especially if you know they are guarded or view discussing money as taboo. Focus on their wishes and on what they want, and be non-judgmental as they open up to you.

What do I ask my parents?

Here are some conversation topics to consider:

“Let’s talk about where you keep your money.” Make sure you understand the whereabouts of your parents’ financial accounts – bank accounts, brokerage accounts, outside investments — so you know who to turn to in case of emergency. Know how much is in the accounts, who has access to them and how they are titled.

“Can you show me where you keep your records?” It may be beneficial for you to make a copy of records such as tax returns, titles to property and insurance policies. Also, make note of the names of their CPA and estate attorney.

“Do you have a safety deposit box at the bank?” Find out what bank they use and where the key is located. Ask how the safety deposit box is titled – is it joint or individual? Find out what is in the box and if any of the items have been appraised.

“Who are your doctors and what prescriptions do you take?” Having a list of their doctors and their contact information will be very helpful in case of emergency. If you live in the same city as your parents, you may have to accompany them to their appointments and be their advocate as they age.

“Do you have a will or estate documents?” Review the following documents with your parents to see if they are prepared: power of attorney (both financial and health care), advanced health care directives, living trust, DNR and a will. Also, discuss if they have any directives regarding specific items that they want passed on or charitable requests to be made.

“Let’s talk about future plans, like long-term care.” Finding out if your parents have long-term care insurance is vital. Those turning 65 today have almost a 70% chance of needing some type of long-term care. Ask them what they expect as they get older: Do they expect a child to be the primary caregiver? Do they want to stay in their home? Do they want to move to an independent living facility that has different levels of care as they progress in age?

What happens if my parents get scammed?

The elderly lose billions of dollars a year to scammers. The question is not whether your parents will be contacted by a scammer, but whether they will be able to recognize the threat when they are contacted. Here are some tips to help you protect them:

Stay connected regularly. Talk to them about the risks of sharing their personal information online, over the phone or by mail. If they think that they have been scammed, have them contact you immediately. They may be embarrassed that this happened to them, but the longer they remain silent, the worse the situation could become.

Set up alerts. They should receive alerts if their account have been hacked or if the bank detects suspicious activity.

Save copies of their correspondence. This will be helpful to share with the authorities, the bank, or credit card companies if they have been scammed.

Encourage an open dialogue. Remember that some people will be ashamed or embarrassed to tell family members that they have been scammed. Remind your parents you are there to help. Show compassion during this stressful time.

Teach digital hygiene. Help them learn to spot suspicious emails, texts and websites. They should look over messages and websites to make sure they are legitimate. They should never share their personal information online or over the phone unless they are certain who they are dealing with. Teach them how to look at an email sender’s address. Discuss that texts they may receive about their password from “Amazon” or “Netflix” are more than likely scams and it is OK to delete them without responding.

It’s important to have a plan in place to address your loved ones’ finances, health and wellness, housing and care and end-of-life plans and wishes. We encourage you to take the first step, if you haven’t already, and open a dialogue with your parents and loved ones. Remember, this is about progress, not perfection. Get the ball rolling, start a conversation, and then keep moving forward.

The CD Wealth Formula

We help our clients reach and maintain financial stability by following a specific plan, catered to each client.

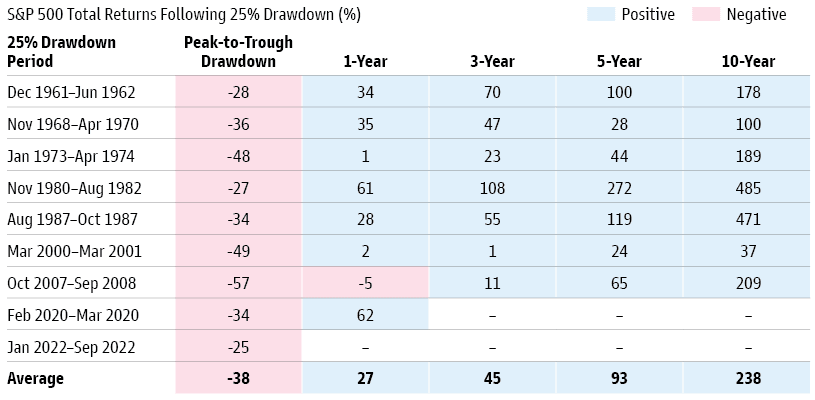

Our focus remains on long-term investing with a strategic allocation while maintaining a tactical approach. Our decisions to make changes are calculated and well thought out, looking at where we see the economy is heading. We are not guessing or market timing. We are anticipating and moving to those areas of strength in the economy — and in the stock market.

We will continue to focus on the fact that what really matters right now is time in the market, not out of the market. That means staying the course and continuing to invest, even when the markets dip, to take advantage of potential market upturns. We continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been.

It is important to focus on the long-term goal, not on one specific data point or indicator. Long-term fundamentals are what matter. In markets and moments like these, it is essential to stick to the financial plan. Investing is about following a disciplined process over time.

Sources: AARP, CNBC, Fidelity, Kiplinger

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. CD Wealth Management and Bluespring Wealth Partners LLC* are affiliates of Kestra IS and Kestra AS. Investor Disclosures: https://bit.ly/KF-Disclosures

*Bluespring Wealth Partners, LLC acquires and supports high quality investment adviser and wealth management companies throughout the United States.