As 2024 draws to a close, we wanted to take this occasion to look back at the articles we’ve produced for our clients so far this year and share the 10 most popular pieces, in case you missed any of them — or if you want to revisit and share them with friends and family.

Every two weeks, we thoughtfully craft these pieces with our clients in mind, broaching subjects we think are relevant and interesting. This is not syndicated content. We want you to find value in these letters — especially in times like these.

1. Understanding How a Living Trust Can Help Your Estate Planning

June 20: A living trust is a flexible, popular tool that allows the estate to avoid probate and lets you control asset distribution after your death. Read more

2. Another Milestone for the Dow: What Could Happen Next?

May 23: The Dow’s rise to 40,000 is a reminder that when it comes to investing, patience is the key. Read more

3. Here’s Why Investors Shouldn’t Panic Over the Market’s New Year’s Hangover

Jan. 12: We talk regularly about not timing the market, and we don’t see these circumstances any differently. Read more

4. Election Advice for Investors: Ignore the Noise, Focus on the Big Picture

Oct. 31: Presidential elections historically have had very little impact on the stock market. Read more

5. What Investors Should Know About This Week’s Market Pullback

Aug. 8: Remember that volatility is normal and that the market does not go up in a straight line. Read more

6. The Market’s Recovery Puts August Pullback in the Rearview Mirror

Aug. 22: More often than any other month, August is when we tend to see out-of-the-blue volatility in the stock market. Read more

7. Here’s How We’re Rebalancing the Portfolio as We Enter the Second Quarter

March 15: We think much of the pain from rising interest rates is behind us — and the key to navigating volatility remains being in a diversified portfolio. Read more

8. Investor Outlook: A Strong May, the First 100 Trading Days and 4 Scams to Watch

June 6: S&P 500 companies are enjoying their best earnings season in almost two years. Read more

9. The Fed’s Next Move: What Could Rate Cuts Mean for Investors?

Sept. 5: Investors who stay only in short-term investments may risk an opportunity to lock in higher yields. Read more

10. How To Make the Biggest Impact With Your Charitable Donation

Sept. 19: Giving can offer a financial benefit for you and your family — as well as the intangible rewards that come with helping others. Read more

The CD Wealth Formula

We help our clients reach and maintain financial stability by following a specific plan, catered to each client.

Our focus remains on long-term investing with a strategic allocation while maintaining a tactical approach. Our decisions to make changes are calculated and well thought out, looking at where we see the economy is heading. We are not guessing or market timing. We are anticipating and moving to those areas of strength in the economy — and in the stock market.

We will continue to focus on the fact that what really matters right now is time in the market, not out of the market. That means staying the course and continuing to invest, even when the markets dip, to take advantage of potential market upturns. We continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been.

It is important to focus on the long-term goal, not on one specific data point or indicator. Long-term fundamentals are what matter. In markets and moments like these, it is essential to stick to the financial plan. Investing is about following a disciplined process over time.

Now that we’re past the halfway point of 2024, we wanted to take this occasion to look back at the articles we’ve produced for our clients so far this year and share the five most popular pieces, in case you missed any of them — or if you want to revisit and share them with friends and family.

Twice a month, we thoughtfully craft these pieces with our clients in mind, broaching subjects we think are relevant and interesting. This is not syndicated content. We want you to find value in these letters — especially in times like these.

+++

1. Understanding How a Living Trust Can Help Your Estate Planning

June 20 | A living trust is a flexible, popular tool that allows the estate to avoid probate and lets you control asset distribution after your death. Read more

+++

2. Another Milestone for the Dow: What Could Happen Next?

May 23 | The Dow’s rise to 40,000 is a reminder that when it comes to investing, patience is the key. Read more

+++

3. Here’s Why Investors Shouldn’t Panic Over the Market’s New Year’s Hangover

Jan. 12 | We talk regularly about not timing the market, and we don’t see these circumstances any differently. Read more

+++

4. Here’s How We’re Rebalancing the Portfolio as We Enter the Second Quarter

March 15 | We think much of the pain from rising interest rates is behind us — and the key to navigating volatility remains being in a diversified portfolio. Read more

+++

5. Investor Outlook: A Strong May, the First 100 Trading Days and 4 Scams to Watch

June 6 | S&P 500 companies are enjoying their best earnings season in almost two years. Read more

+++

P.S. Looking for more? Here are the five articles that are most popular this year on our website (no matter when they were published).

We help our clients reach and maintain financial stability by following a specific plan, catered to each client.

Our focus remains on long-term investing with a strategic allocation while maintaining a tactical approach. Our decisions to make changes are calculated and well thought out, looking at where we see the economy is heading. We are not guessing or market timing. We are anticipating and moving to those areas of strength in the economy — and in the stock market.

We will continue to focus on the fact that what really matters right now is time in the market, not out of the market. That means staying the course and continuing to invest, even when the markets dip, to take advantage of potential market upturns. We continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been.

It is important to focus on the long-term goal, not on one specific data point or indicator. Long-term fundamentals are what matter. In markets and moments like these, it is essential to stick to the financial plan. Investing is about following a disciplined process over time.

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. CD Wealth Management and Bluespring Wealth Partners LLC* are affiliates of Kestra IS and Kestra AS. Investor Disclosures: https://bit.ly/KF-Disclosures

*Bluespring Wealth Partners, LLC acquires and supports high quality investment adviser and wealth management companies throughout the United States.

Fidelity Investments and Fidelity Institutional® (together “Fidelity”) is an independent company, unaffiliated with Kestra Financial or CD Wealth Management. Fidelity is a service provider to both. There is no form of legal partnership, agency affiliation, or similar relationship between your financial advisor and Fidelity, nor is such a relationship created or implied by the information herein. Fidelity has not been involved with the preparation of the content supplied by CD Wealth Management and does not guarantee, or assume any responsibility for, its content. Fidelity Investments is a registered service mark of FMR LLC. Fidelity Institutional provides clearing, custody, or other brokerage services through National Financial Services LLC or Fidelity Brokerage Services LLC, Members NYSE, SIPC.

As 2023 nears its end, we wanted to take this occasion to look back at the articles we’ve produced for our clients so far this year and share the 10 most popular pieces, in case you missed any of them — or if you want to revisit and share them with friends and family.

Every week, we thoughtfully craft these pieces with our clients in mind, broaching subjects we think are relevant and interesting. This is not syndicated content. We want you to find value in these letters — especially in times like these.

1. A New Bull Market Has Begun — Here’s What Investors Should Know

June 15: The S&P 500 closed more than 20% higher than its October low. For now, the 2022 bear market is over. Read more

2. 2023 at the Halfway Point: Where We’ve Been and What Lies Ahead

June 22: Here are some of the key indicators and trends we are watching for the second half of the year. Read more

3. Here Are the Portfolio Changes We’re Making as We Near the End of the Year

Nov. 9: The world in which interest rates stay higher for longer is not one we have been accustomed to for the last 15 years. Read more

4. The RMD Deadline Is Right Around the Corner — Are You Prepared?

Oct. 26: It is important to understand your options to maximize your income and avoid a costly tax mistake. Read more

5. Here’s Why Patience May Be an Investor’s Greatest Asset

Sept. 21: There will always be reasons to worry about the market, but not doing anything can be a very powerful choice. Read more

6. Understanding the 10-Year Treasury and Why It Matters to Investors

Nov. 2: The rising yield can be a barometer for interest rates on mortgages, student loans and other forms of borrowing. Read more

7. The Portfolio Changes We’re Making as We Enter the Third Quarter of 2023

June 29: The market is watching to see if a recession unfolds, caused by interest rate hikes, inflation and remaining effects of the banking crisis. Read more

8. Turning Investment Losses into Gains: The Art of Tax-Loss Harvesting

Oct. 20: Not every investment will be a winner, but sometimes an investment that has lost money can still do some good. Read more

9. What Does the Fed’s ‘Higher-for-Longer’ Stance Mean for Investors?

Sept. 28: The Fed is working hard not to allow inflation to rear its head again, after it has steadily declined over the last six months. Read more

10. Don’t Wait Until Retirement to Learn About Medicare — Here’s What You Should Know

July 20: For many people, the cost of healthcare is the biggest unknown for retirement planning. Read more

The CD Wealth Formula

We help our clients reach and maintain financial stability by following a specific plan, catered to each client.

Our focus remains on long-term investing with a strategic allocation while maintaining a tactical approach. Our decisions to make changes are calculated and well thought out, looking at where we see the economy is heading. We are not guessing or market timing. We are anticipating and moving to those areas of strength in the economy — and in the stock market.

We will continue to focus on the fact that what really matters right now is time in the market, not out of the market. That means staying the course and continuing to invest, even when the markets dip, to take advantage of potential market upturns. We continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been.

It is important to focus on the long-term goal, not on one specific data point or indicator. Long-term fundamentals are what matter. In markets and moments like these, it is essential to stick to the financial plan. Investing is about following a disciplined process over time.

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. CD Wealth Management and Bluespring Wealth Partners LLC* are affiliates of Kestra IS and Kestra AS. Investor Disclosures: https://bit.ly/KF-Disclosures

*Bluespring Wealth Partners, LLC acquires and supports high quality investment adviser and wealth management companies throughout the United States.

Fidelity Investments and Fidelity Institutional® (together “Fidelity”) is an independent company, unaffiliated with Kestra Financial or CD Wealth Management. Fidelity is a service provider to both. There is no form of legal partnership, agency affiliation, or similar relationship between your financial advisor and Fidelity, nor is such a relationship created or implied by the information herein. Fidelity has not been involved with the preparation of the content supplied by CD Wealth Management and does not guarantee, or assume any responsibility for, its content. Fidelity Investments is a registered service mark of FMR LLC. Fidelity Institutional provides clearing, custody, or other brokerage services through National Financial Services LLC or Fidelity Brokerage Services LLC, Members NYSE, SIPC.

As we begin to wrap up the year, it is the perfect time to review year-end planning strategies to ensure that your wealth plan reflects any changes in your circumstances or goals, the current tax environment and the economic landscape. The end of the year is an important time for making financial decisions that can have an impact not only in the new year ahead, but for years to come.

Here are a few high-level takeaways from 2023:

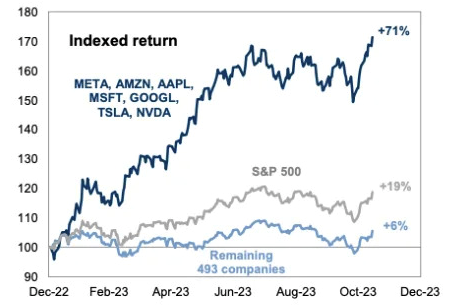

The Magnificent 7 Roar Ahead

Amazon, Apple, Google (Alphabet), Meta, Microsoft, Nvidia and Tesla make up 29% of the S&P 500 market cap and have driven most of the U.S. stock market performance in 2023. Remember: These same stocks were down over 45% on average in 2022. For those investors who didn’t panic and held onto these stocks, patience paid off.

Sources: FactSet, Goldman Sachs Global Investment Research

Recession or No Recession?

This year may be remembered for the most anticipated recession in history that didn’t happen. Investors fluctuated on when and if a recession may occur. What we did see was recessions in different sectors, such as commercial real estate and housing, but not for the overall economy.

The Fed vs. Inflation

The Federal Reserve hiked interest rates an additional four times in 2023, with the Fed Funds rate ending the year at 5.25%, a 22-year high. The old mantra of “Don’t fight the Fed” gave way to “higher interest rates for longer.” The Fed has reiterated all year that its inflation target is 2% and that it will do what it needs to do to bring inflation down.

The Rise of AI

Artificial Intelligence has captured investors’ minds and has contributed to the outperformance of both the Magnificent 7 and technology stocks as a whole. During second-quarter earnings calls, 35% of companies in the S&P 500 mentioned AI. This moderated some in the third quarter as only 29% of companies discussed AI, but very strong momentum remains heading into 2024.

Earning Money on Cash

Money market yields reached their highest levels since 2007 with the Fed raising the Fed funds rate. For fixed-income investors, returns on Treasuries, CDs and bonds provided attractive levels to lock in higher yields for longer.

Year-End Checklist

As we near 2024, we recommend that you review the checklist below for planning strategies to consider and discuss.

Income Tax Strategies

• Traditional year-end planning focuses on deferring income to a future year and accelerating deductions into the current year.

• If you anticipate that your marginal income tax bracket will increase, you may consider accelerating income into 2023 and deferring deductions to 2024.

• If you anticipate being in a lower tax bracket next year: — Defer income if possible in order to postpone paying the tax and have that income at a lower bracket. — If you itemize on your tax return, bunch your medical expenses in the current year to meet the percentage of your adjusted gross income to claim those deductions. — Make your January mortgage payment in December so that you can deduct the interest on this year’s return.

Tax-Related Investment Strategies

• Tax-loss harvesting is the strategy of selling securities at a loss to offset a capital gain liability, either for today or in the future. — Harvest losses by selling taxable investments. (You must wait at least 31 days before buying back a holding sold for a loss to avoid the IRS wash-sale rule.) — Harvest gains by selling taxable investments if you have a tax loss carryforward.

• Ensure that you have satisfied your required minimum distributions (RMD). — If you fail to take your RMD, this may result in a 50% penalty. — If you own an inherited IRA, an RMD may be required separately for that account as well.

Retirement Planning Strategies

• Maximize your IRA contributions. You may be able to deduct annual contributions of up to $6,500 to your traditional IRA and $6,500 to your spouse’s IRA ($7,500 if over age 50).

• Make a Roth IRA contribution if under the applicable income limits.

• Consider increasing or maximizing your 401(k) contribution. This year, the maximum contribution is $22,500 for those under 50 and $30,000 for those over the age of 50. Boosting contributions to your 401(k) can lower your adjusted gross income while increasing your retirement savings.

• Consider making contributions to a Roth 401(k) if your plan allows.

• Consider setting up a Roth IRA for each of your children who have earned income during the year.

Gifting Strategies

• Consider making gifts up to $17,000 per person as allowed under the federal annual gift tax exclusion. You can give up to $17,000 this year to as many people as you want without triggering gift taxes. Payments made directly to educational and/or medical institutions on behalf of your intended beneficiary do not count towards your annual exclusion amount or against your lifetime estate tax exclusion.

• Create a donor advised fund for an immediate income tax deduction and provide immediate and future benefits to charity over time.

• If you already have a donor advised fund or want to donate to a charity, consider gifting appreciated assets that have been held longer than one year to get the fair market value income tax deduction while avoiding income tax on the appreciation.

• If you are over the age of 70½, consider making a direct transfer from an IRA to a public charity. The distribution is excluded from gross income, and you can give up to $100,000 as a tax-free gift from your IRA, which may fully satisfy RMD requirements.

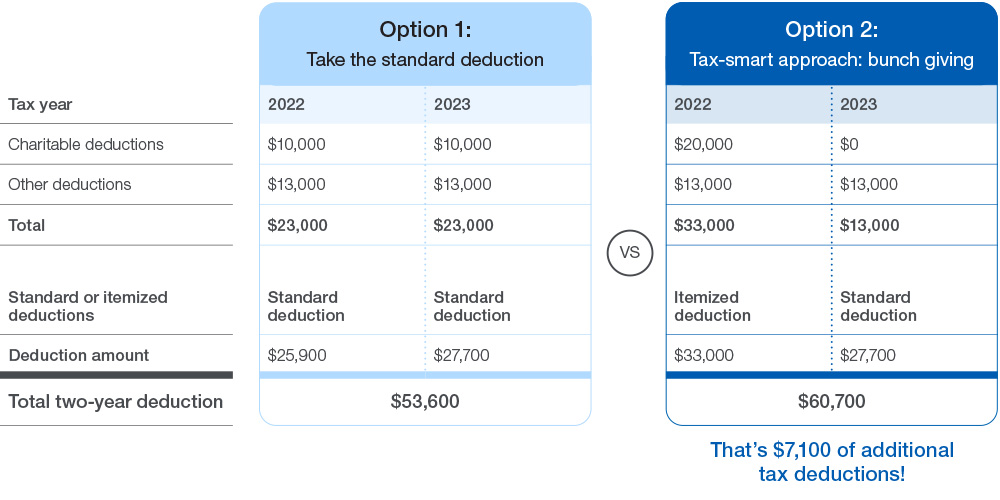

• Consider combining multiple years of charitable giving into a single year to exceed the standard deduction threshold. This is called “bunching.” The chart below reflects the bunching strategy and how it can reduce taxes if executed properly.

Wrapping Up 2023, Planning for 2024

• Discuss major life events with CD Wealth Management to confirm you have clarity in your current situation.

• Communicate with your CPA to provide capital gains and investment income information for a more accurate year-end projection.

• Check your Health Savings Account (HSA) contributions for 2023. If you qualify, you can contribute up to $3,850 (individual) or $7,750 (family) — and an additional $1,000 catch-up if you are over the age of 55.

• Double-check your beneficiary designations for retirement plans, IRAs, Roth IRAs, annuities, life insurance policies, etc.

• If you do not already have identity theft protection, consider purchasing a service to help protect you and your family.

The end of the year is a perfect time to review your financial planning needs, including reviewing the investment portfolio, assessing year-end tax planning opportunities, reviewing retirement goals and managing your legacy plans.

The checklist above includes just some of the items that may apply to you and your family. We are happy to meet to discuss any of the above to ensure that you remain on track with your financial goals.

The CD Wealth Formula

We help our clients reach and maintain financial stability by following a specific plan, catered to each client.

Our focus remains on long-term investing with a strategic allocation while maintaining a tactical approach. Our decisions to make changes are calculated and well thought out, looking at where we see the economy is heading. We are not guessing or market timing. We are anticipating and moving to those areas of strength in the economy — and in the stock market.

We will continue to focus on the fact that what really matters right now is time in the market, not out of the market. That means staying the course and continuing to invest, even when the markets dip, to take advantage of potential market upturns. We continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been.

It is important to focus on the long-term goal, not on one specific data point or indicator. Long-term fundamentals are what matter. In markets and moments like these, it is essential to stick to the financial plan. Investing is about following a disciplined process over time.

Sources: FactSet, Goldman Sachs, Schwab

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. CD Wealth Management and Bluespring Wealth Partners LLC* are affiliates of Kestra IS and Kestra AS. Investor Disclosures: https://bit.ly/KF-Disclosures

*Bluespring Wealth Partners, LLC acquires and supports high quality investment adviser and wealth management companies throughout the United States.

Fidelity Investments and Fidelity Institutional® (together “Fidelity”) is an independent company, unaffiliated with Kestra Financial or CD Wealth Management. Fidelity is a service provider to both. There is no form of legal partnership, agency affiliation, or similar relationship between your financial advisor and Fidelity, nor is such a relationship created or implied by the information herein. Fidelity has not been involved with the preparation of the content supplied by CD Wealth Management and does not guarantee, or assume any responsibility for, its content. Fidelity Investments is a registered service mark of FMR LLC. Fidelity Institutional provides clearing, custody, or other brokerage services through National Financial Services LLC or Fidelity Brokerage Services LLC, Members NYSE, SIPC.

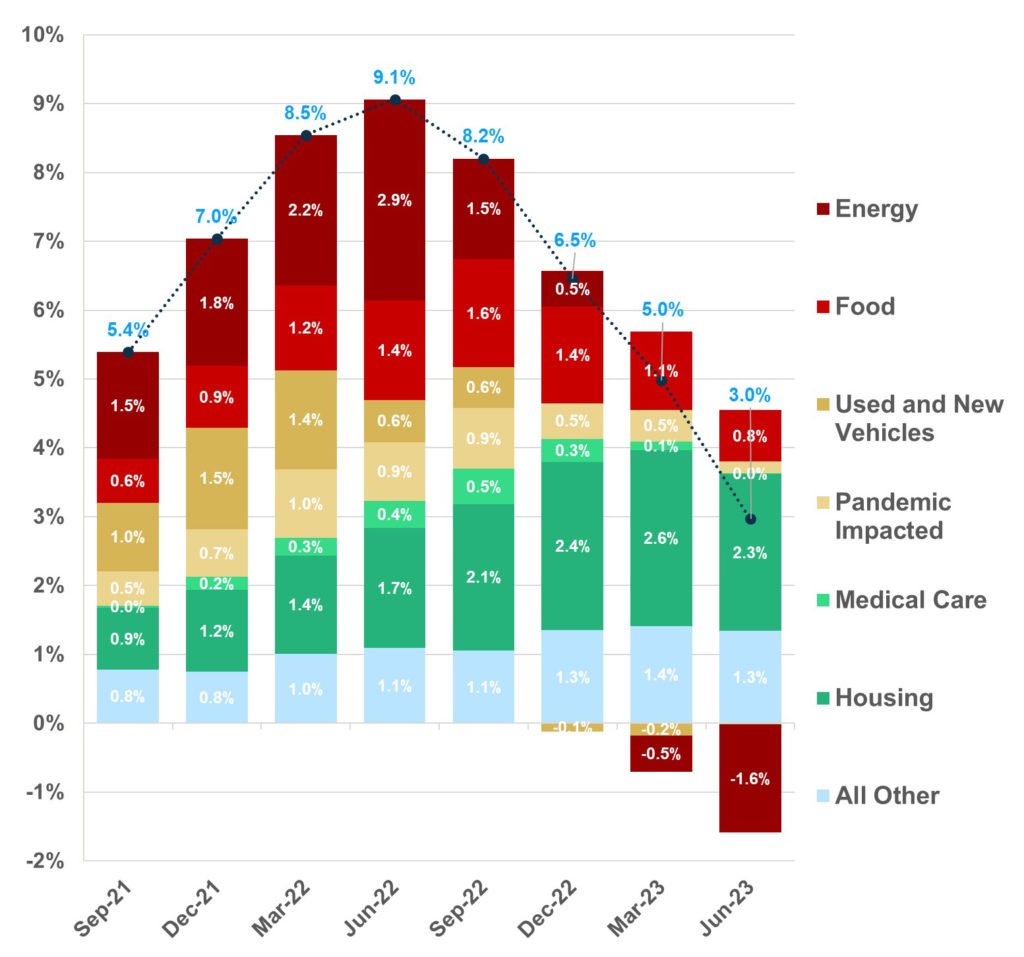

Inflation continues to come down after reaching a peak of 9.1% in June 2022 — a far cry from the high inflation days of the early 1980s, but levels we hadn’t seen in 40 years nonetheless. June’s Consumer Price Index (CPI) came in at an annualized rate of 3%, the lowest level since March 2021 and the 12th consecutive month of price decreases. The CPI remains above the Fed’s target rate of 2%, and while this report is good news for prices and pocketbooks, it is unlikely to stop the Fed from raising rates again later this month. Energy prices also are decreasing; gas was $5 a gallon at this time last year, and price increases were at their highest levels.

Inflation Pulls Back on Lower Energy, Food and Used Car Prices

Contributions to CPI Inflation (Year-Over-Year)

Data source: Carson Investment Research, BLS 7/12/2023. Pandemic-impacted categories include car and truck rentals, furnishings and supplies, apparel, airline fares, lodging away from home including hotels and motels. Housing includes rent of primary residence and owners’ equivalent rent. Medical care includes medical care commodities and services. @sonusvarghese

The largest increase in inflation remains healthcare, which is up significantly since the start of the pandemic. For many people, the cost of healthcare is the biggest unknown for retirement planning. How long will I live? What medical needs will I have? Do I need long-term care coverage, and what will that pay for? Do I have enough money to pay for my healthcare needs as I get older, or will I have to depend on my kids or other family members?

Luckily for those who are about to turn 65 — or who are already older than 65 — there is Medicare, which includes several different forms of health care, some provided by the federal government and some by private insurers. Medicare can be complicated to understand, but it is important to know your options.

When do I sign up for Medicare?

The initial enrollment period is a seven-month period around the time you turn 65 and includes the three full months before the month you turn 65, the month you turn 65 and the three full months after the month you turn 65.

There are exceptions to the window for those who are still working and opportunities to enroll later in life. In some cases, though, you can end up paying higher rates by waiting.

What does Medicare entail?

Medicare consists of five major parts:

• Part A covers hospital and skilled nursing care, as well as some home and hospice care. As soon as you turn age 65, you are eligible for Part A, usually at no cost. At age 65, most individuals opt into Part A at a minimum. The main downside is that you are no longer eligible to contribute to a health savings plan if you chose Part A.

• Part B covers outpatient care, such as office visits, diagnostics and some preventative services. If you are on Social Security, you are automatically enrolled in Part B, which has a monthly premium that varies based on your income. If you are still working, you can decline Part B. Once you retire and lose your work insurance, you have an eight-month special enrollment period to sign up for part B.

• Part D is your drug plan that’s offered by private insurers. They require a separate premium that is regulated by the government. There are a wide variety of plans, so shopping to make sure you get the right one is important.

• Part C, also called Medicare Advantage, offers hospital and medical coverage along with benefits you do not get with basic Medicare, like vision, hearing and prescription drugs. Part C is offered through private insurers, and the out-of-pocket expense is capped by the government. If you chose Part C, you will probably not need Part D.

• Medigap Coverage is technically not part of Medicare, but it is commonly purchased as a supplement to Medicare. It is sold by private insurers to cover some costs that Medicare doesn’t, like copayments and deductibles.

What does Medicare not cover?

Medicare does not cover everything, and you will need to pay for or obtain other coverage as mentioned above for services that are not included. Some of the items and services Medicare does not cover are:

• Long-term care • Most dental care • Eye exams • Dentures • Cosmetic surgery • Routine physical exams • Hearing aids • Concierge services

Medicare & You, the official U.S. government Medicare handbook, contains much more detailed information. (This is a good link to bookmark for future reference.)

If I am not eligible yet, what should I do?

As you approach age 65, mark your calendar for the specific date that you would like to enroll. If you are still working, it may make sense to enroll in Part A only and continue with your company insurance.

Take time to research Medicare plans to match your specific needs. At CD Wealth Management, we think this is an important part of your retirement and should be something you review each year.

The CD Wealth Formula

We help our clients reach and maintain financial stability by following a specific plan, catered to each client.

Our focus remains on long-term investing with a strategic allocation while maintaining a tactical approach. Our decisions to make changes are calculated and well thought out, looking at where we see the economy is heading. We are not guessing or market timing. We are anticipating and moving to those areas of strength in the economy — and in the stock market.

We will continue to focus on the fact that what really matters right now is time in the market, not out of the market. That means staying the course and continuing to invest, even when the markets dip, to take advantage of potential market upturns. We continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been.

It is important to focus on the long-term goal, not on one specific data point or indicator. Long-term fundamentals are what matter. In markets and moments like these, it is essential to stick to the financial plan. Investing is about following a disciplined process over time.

Sources: Blackrock, Bloomberg, Carson, Schwab

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. CD Wealth Management and Bluespring Wealth Partners LLC* are affiliates of Kestra IS and Kestra AS. Investor Disclosures: https://bit.ly/KF-Disclosures

*Bluespring Wealth Partners, LLC acquires and supports high quality investment adviser and wealth management companies throughout the United States.

Fidelity Investments and Fidelity Institutional® (together “Fidelity”) is an independent company, unaffiliated with Kestra Financial or CD Wealth Management. Fidelity is a service provider to both. There is no form of legal partnership, agency affiliation, or similar relationship between your financial advisor and Fidelity, nor is such a relationship created or implied by the information herein. Fidelity has not been involved with the preparation of the content supplied by CD Wealth Management and does not guarantee, or assume any responsibility for, its content. Fidelity Investments is a registered service mark of FMR LLC. Fidelity Institutional provides clearing, custody, or other brokerage services through National Financial Services LLC or Fidelity Brokerage Services LLC, Members NYSE, SIPC.

No one likes tax season, but there are some steps you can take to reduce the headaches and make things easier for you and your CPA. Your preparer should tell you when they need all the information to finalize or to extend your return before the deadline. If you are asked to complete a questionnaire, there’s a reason why: Those documents cover most (if not all) of what you will need to provide for your return to be complete and accurate.

Most of life’s major events seem to have a tax impact: marriage, divorce, births, deaths, home purchase or sale, new business, inheritance, etc. Your preparer’s questionnaire is designed to ensure you don’t forget to include anything important. Be sure to review all the questions they ask, as things change from year to year.

As we approach April 15, here are some ways to make tax season go more smoothly — and a list of documents you might need.

Documentation Reported to IRS

• W-2s: If you work for an employer, you will have a W-2 that shows how much you earned and how much was deducted for taxes and other withholdings. • 1099-NEC (MISC): If you are a contract employee, you can expect to receive this form. • 1099-INT and 1099-DIV: If you earned interest from savings or investments, you may receive this form. The 1099-DIV reports dividends and distributions from investments. Sources for 1099s include bank interest, brokerage accounts, stock dividends and sales, sale of real estate, Social Security and 529 distributions, to name a few. • Consolidated 1099: This brokerage tax form will show income from dividends, both qualified and non-qualified, as well as any capital gains and losses that occurred during the year. • 1099-R: If you take a distribution from your retirement account, you will have a 1099-R that shows the amount of distribution and amount of taxes withheld. • 5498: This form reports your total annual contributions to an IRA account and identifies the type of retirement account you have. • 1098: If you own a home and pay mortgage interest, you will receive this form from your lender, showing the amount of interest that was paid and that can be deducted. • 1098-T: If you have a dependent in college, you will receive this form that reports how much qualified tuition and expense was paid during the year. • K-1: If you have any limited partner investments, you will receive a K-1 that shows each partner’s share of the partnership’s earnings, losses, deductions and credits. Examples include trusts, partnerships, and S Corporations.

Information Not Reported to the IRS That Requires Recordkeeping

• Business income and expenses. • Charitable contributions, including donor-advised funds and qualified charitable distributions. Remember, when you make a donation to a qualified charity from a donor-advised fund or from your IRA (if you are over age 70½), you are not eligible for a charitable deduction at that time. You received a deduction when you added monies to the donor-advised fund, and you are reducing your taxable income when made from the IRA. • Real estate taxes. • Contributions to 529s, HSAs and IRAs. • Medical expenses. • Estimated tax payments.

Old Files You Should Retain

• In most cases, you should plan on keeping tax returns — along with W-2s, 1099s, records supporting itemized deductions and other documents — for a period of at least three years following the date you filed or the due date of your tax return. • Keeping tax returns for the three-year period is tied to the IRS statute of limitations. The IRS generally has only three years from the filing date or due date of the return to assess additional taxes. • In some cases, you may need to hold onto your records longer than three years: — Keep tax forms for retirement accounts, such as IRAs, until seven years after the account is zeroed out. — If you file a claim for worthless security or bad debt, you must keep those records for seven years. — If you buy or sell property, you should keep property records until the statute of limitations expires for the year in which you disposed of the property.

Maintaining good records and approaching tax season efficiently can have other benefits; being proactive and comprehensive can help you minimize taxes. Along with your CPA, CD Wealth Management can help you develop tax strategies that will pay off now — and well into the future. Once you have filed your taxes, it is beneficial to provide your financial advisor with a copy of your return.

Remember, tax planning is not just a once-a-year event. We want to ensure you that we are evaluating the landscape for tax changes and strategies that may help save future dollars and keep money in your pocket.

The CD Wealth Formula

We help our clients reach and maintain financial stability by following a specific plan, catered to each client.

Our focus remains on long-term investing with a strategic allocation while maintaining a tactical approach. Our decisions to make changes are calculated and well thought out, looking at where we see the economy is heading. We are not guessing or market timing. We are anticipating and moving to those areas of strength in the economy — and in the stock market.

We will continue to focus on the fact that what really matters right now is time in the market, not out of the market.

That means staying the course and continuing to invest, even when the markets dip, to take advantage of potential market upturns. We continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been.

It is important to focus on the long-term goal, not on one specific data point or indicator. Long-term fundamentals are what matter. In markets and moments like these, it is essential to stick to the financial plan. Investing is about following a disciplined process over time.

Sources: IRS, Carson, Baird

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. CD Wealth Management and Bluespring Wealth Partners LLC* are affiliates of Kestra IS and Kestra AS. Investor Disclosures: https://bit.ly/KF-Disclosures

*Bluespring Wealth Partners, LLC acquires and supports high quality investment adviser and wealth management companies throughout the United States.

We wanted to take this occasion to look back at the content we’ve produced this year and share the 10 most widely read pieces of 2022 in case you missed any of them — or if you want to revisit and share them with friends and family.

Every week, we thoughtfully craft these letters with our clients in mind, broaching subjects we think are relevant and interesting. This is not syndicated content. We want you to find value in these letters — especially in times like these.

1. Before You Sell for a Loss, Make Sure You Know the Wash-Sale Rule

Investors may have seller’s remorse, but capturing losses to offset current taxes or future gains is a prudent strategy | May 5

When you sell an investment that has a loss in a taxable account, you may be eligible for a tax benefit. The wash-sale rule prevents investors from selling at a loss, then buying back the “substantially identical” investment within a 61-day window and being able to claim the tax benefit. This rule applies to stocks, bonds, mutual funds, exchange traded funds (ETFs) and options. Read more >

2. Midterm Elections are Right Around the Corner. What Does This Mean for the Market?

Midterm election years are historically more volatile than the rest of the presidential cycle | July 21

Depending on which party controls Congress, U.S. fiscal policy may change after the election. However, economic fundamentals — and not election results — play the greatest role in stock market performance. Read more >

3. Understanding the Importance of Market Liquidity

As the Fed injects less money into the economy to slow down inflation, liquidity is being reduced, which can lead to outsized market moves | Feb. 10

Over the last few years, liquidity has been a major driver in the stock market. In a liquid market — one that is not dominated by selling — the bid price and ask price are close to each other. As a market becomes more illiquid, such as during a sell-off like we saw last month, the spread between the bid and ask prices grows — meaning prices become less stable and transparent. Read more >

4. Here’s Why Today’s Housing Market Is Different from 2008

Home prices are rising, but the underlying drivers of the current market are different from the Great Financial Crisis | July 1

Lending has been in favor of those with much higher credit scores. Household balance sheets are in much better shape, and the percentage of one’s disposable income spent on mortgages is at an all-time low. Read more >

5. The Case for Staying Invested, Even When the Market Declines

The instinct to flee when the market starts to fall can have a major negative impact on the portfolio’s long-term health | Feb. 17

Investors who sit on the sidelines risk losing out on periods of market appreciation that follow the downturns. From 1929 through 2020, every decline of 15% or more in the S&P 500 has been followed by a strong recovery. Read more >

6. Don’t Let the Word ‘Recession’ Scare You: Here’s What History Has to Say

Recessions are normal occurrences in the economic cycle. In fact, we’ve already had three this century. Here’s what you should know | June 10

Just because the U.S. economy may have a recession does not mean it will be 2008 all over again and the stock market will experience similar pain. The stock market is a leading economic indicator, but most often it has already started to recover by the time the economy is officially in recession. Read more >

7. You’ve Inherited an IRA. What Happens Next?

The SECURE Act effectively ended the Stretch IRA, but it did not eliminate the need for financial planning when it comes to distributions | April 14

Under current law, you have 10 years to deplete the entire value of the IRA. However, if you wait until the 10th year to take the entire distribution and the IRA has experienced significant growth, you may be in the highest tax bracket, having to pay almost 40% in taxes for that one year. Read more >

8. What You Need to Know About Web 3.0 and the Metaverse

Social attitudes and norms are changing and adapting to the new era of the internet | Jan. 20

It will take many years for the metaverse to be fully formed and for the experiences to become part of the daily world. However, it appears the train has left the station, with social media and video game companies leveraging their large user bases to build the foundation of the metaverse. Read more >

9. What Does a Stronger U.S. Dollar Mean for You?

For the first time in nearly two decades, the exchange rate between the euro and the dollar is roughly the same | July 14

The parity in the two currencies comes after the euro has plunged almost 20% in value over the last 14 months compared to the dollar. This year, the U.S. dollar has gained against most major currencies, as the Fed’s interest rate hikes have made the dollar a safe haven for investors worldwide who are seeking protection against surging global inflation. Read more >

10. An Introduction to NFTs: What You Should Know About Digital Art

Like any collectible, an NFT’s value is based entirely on what someone else is willing to pay for it | Feb. 24

There are tens of thousands of NFTs in existence, representing a variety of topics, such as music, art and sports. Like any piece of art, beauty is in the eye of the beholder. Read more >

The CD Wealth Formula

We help our clients reach and maintain financial stability by following a specific plan, catered to each client.

Our focus remains on long-term investing with a strategic allocation while maintaining a tactical approach. Our decisions to make changes are calculated and well thought out, looking at where we see the economy is heading. We are not guessing or market timing. We are anticipating and moving to those areas of strength in the economy — and in the stock market.

We will continue to focus on the fact that what really matters right now is time in the market, not out of the market. That means staying the course and continuing to invest, even when the markets dip, to take advantage of potential market upturns. We continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been.

It is important to focus on the long-term goal, not on one specific data point or indicator. Long-term fundamentals are what matter. In markets and moments like these, it is essential to stick to the financial plan. Investing is about following a disciplined process over time.

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. CD Wealth Management and Bluespring Wealth Partners LLC* are affiliates of Kestra IS and Kestra AS. Investor Disclosures: https://bit.ly/KF-Disclosures

*Bluespring Wealth Partners, LLC acquires and supports high quality investment adviser and wealth management companies throughout the United States.

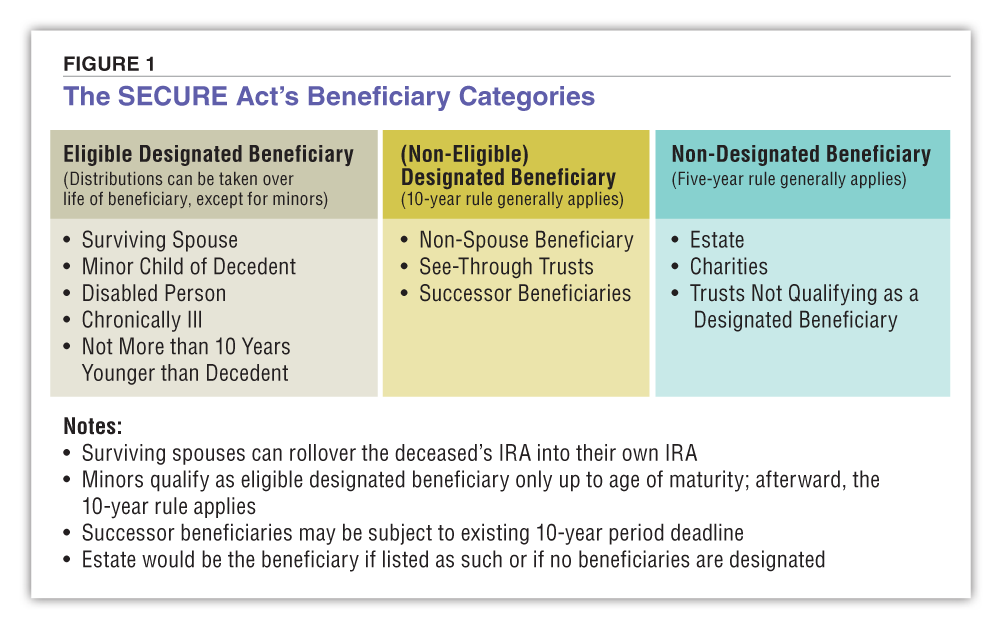

Prior to December 2019, if you inherited an IRA from someone who was not your spouse, you were able to take distributions from the inherited account based on your life expectancy and not the original owner’s, a strategy commonly known as a Stretch IRA. The benefit of using a Stretch IRA was that the beneficiary could stretch the taxable distributions over their lifetime, which potentially meant a lower tax bill. The rules were the same for a Roth IRA; even though the original Roth IRA owners did not have required minimum distributions, their heirs were required to withdraw the funds according to their life expectancy.

Under current tax law, the inheritance of an IRA is tax-free, but you are still required to take distributions from the account that may be taxable. When you inherit an IRA, you are free to withdraw as much of the account as you want at any time without penalty.

Stretch IRA rules changed with the passage of the SECURE Act in December 2019, however. The SECURE Act mandates that an IRA inherited from someone who is not your spouse must be depleted by Dec. 31 after the 10th anniversary of the owner’s death. For example: If you inherit an IRA this year, you will have to distribute the balance of the account by Dec. 31, 2032.

Spousal IRA beneficiaries have different rules and more options to consider when taking their required minimum distributions. As the chart below indicates, there are exceptions to the 10-year rule, such as a surviving spouse, a disabled or chronically ill person, a minor or a person who is not more than 10 years younger than the IRA account owner. These beneficiaries are not obligated to empty the IRA within 10 years but still must take their distributions. If you fall into the eligible designated beneficiary category, the inherited IRA can be taken over the life of the beneficiary (except in the case of minors). If you are a non-eligible designated beneficiary, such as someone who inherits an IRA from a parent, the 10-year rule applies.

What does this mean for me?

If you inherit an IRA and are a non-eligible beneficiary, planning for taxes and how you take distributions becomes more important. Under current law, you have 10 years to deplete the entire value of the IRA. However, if you wait until the 10th year to take the entire distribution and the IRA has experienced significant growth, you may be in the highest tax bracket, having to pay almost 40% in taxes for that one year. If you take distributions over the 10 years, you may incur less tax on an annual basis, and the potential growth of the IRA may be minimized as well. As we have previously written, another way to potentially reduce taxes is to transfer up to $100,000 from an IRA directly to a qualified charity if you are 70 ½ or older.

The IRS has proposed new regulations to the SECURE Act which have yet to be approved. The proposed changes state that if you inherit a traditional IRA from someone who has already passed their required beginning date and had been taking mandatory distributions, you cannot wait until the 10th year to withdraw the money. Instead, under the proposal, you would be required take annual distributions in the first nine years and the balance in the 10th. A tax liability would occur each year from the required distribution.

The SECURE Act has brought Roth conversions into the conversation for those who want to help their heirs avoid a large tax bill. Roth conversions transfer the tax liability to the older generation, because taxes are paid when the conversion is done. If the conversion is done early in retirement, when income is low, the tax bracket may be lower and thus, lower taxes would be paid on the Roth conversion. Then the money can grow tax-free inside the Roth IRA and when the owner passes away, the money can continue to grow tax-free for an additional 10 years.

So, what can we learn from all this? While the SECURE Act effectively eliminated the Stretch IRA, it did not eliminate the need for proper financial planning when it comes to taking distributions from an inherited IRA. We will continue to closely watch proposed legislation about the 10-year rule for inherited IRAs and ensure that our clients take the necessary distributions, if mandated by law. In the interim, we continue to analyze your situation and help you determine what makes the most sense for taxes, investments and your overall financial plan for IRA distributions.

From a portfolio perspective, we continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been. As we say each week, it is important to stay the course and focus on the long-term goal, not on one specific data point or indicator. In markets and moments like these, it is essential to stick to the financial plan.

Remember first and foremost that panic is not an investing strategy. Neither are “get in” or “get out” — those are just gambling on moments in time. Investing is about following a disciplined process over time.

At the end of the day, investors will be well-served to remove emotion from their investment decisions and remember that over a longer time horizon, markets tend to rise. Market corrections are normal, as nothing goes up in a straight line. Making market decisions based on what might happen may be detrimental to long-term performance. The key is to stay invested and stick with the financial plan. Markets go up and down over time, and downturns present opportunities to purchase stocks at a lower value.

It all starts with a solid financial plan for the long run that understands the level of risk that is acceptable for each client. Regarding investments, we believe in diversification and having different asset classes. The best option is to stick with a broadly diversified portfolio that can help you to achieve your own specific financial goals — regardless of market volatility. Long-term fundamentals are what matter.

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. CD Wealth Management and Bluespring Wealth Partners LLC* are affiliates of Kestra IS and Kestra AS. Investor Disclosures: https://bit.ly/KF-Disclosures

*Bluespring Wealth Partners, LLC acquires and supports high quality investment adviser and wealth management companies throughout the United States.

Increasingly, families depend on the income of two working parents. If you’re a working mother, your income can have a significant impact on the quality of your family’s lifestyle. Your income helps cover the cost of ordinary living expenses such as food, clothing, and utilities, and it provides savings for your children’s college education, and for your retirement. Life insurance protects your family by providing proceeds that can be used to replace your lost income if you die prematurely.

Single women

Often, women, like men, think that it’s not necessary to buy life insurance because they have no dependents. What’s often overlooked is that life insurance can provide necessary funds to pay off car loans, education loans, debts, a mortgage, taxes, and funeral expenses that might otherwise be the responsibility of family members. Also, the cash value of permanent life insurance may be used to supplement retirement income.

Single moms

Whether you’re divorced, widowed, or simply a single mom, you’re most likely primarily responsible for your child’s support. If you die prematurely, life insurance can provide ongoing income to cover child-care costs, medical expenses, debts, and future college costs.

If you die, your surviving spouse may have to pay for services such as child care, transportation for your children, and housekeeping. Proceeds from your life insurance can help your spouse pay for services that keep the household running and allow your spouse to keep working.

Stay-at-home moms

Maintaining a household is a full-time job, and you have many important roles and duties. The cost of the services performed by a stay-at-home mom could be quite significant if someone had to be hired to do them. If you die, your surviving spouse may have to pay for services such as child care, transportation for your children, and housekeeping. Taking over these added responsibilities could cause your spouse to shorten work hours, resulting in a reduction in income. Proceeds from your life insurance can help your spouse pay for services that keep the household running and allow your spouse to keep working.

Family caregiver

Many women find themselves providing care for both children and elderly family members. Caring for an aging parent or family member can include paying for the costs of adult day care, uninsured medical expenses, and extra transportation. Adding these expenses to the costs of maintaining a household, child care, and college tuition can be financially overwhelming. Unfortunately, these added financial responsibilities often continue after your death. Life insurance provides a source of funds that can be used to help pay for these expenses.

Business owner

You may be one of the increasing number of women business owners. If you die while owning your business, life insurance can be used to provide cash for company expenses such as payroll or operating costs while your estate is being settled. Also, life insurance can be a useful tool for business owners structuring buy-sell arrangements or providing benefits to key employees.

Life insurance types and options

Life insurance comes in many different sizes and shapes, and determining the policy that meets your needs may depend on a number of factors. Understanding the basic types of life insurance can help you find the policy that’s appropriate for you.

Term life insurance

Term life insurance provides a simple death benefit for a specified period of time. If you die during the coverage period, the beneficiary you name in the policy receives the death benefit. If you live past the term period, your coverage ends, and you get nothing back. The cost, or premium, for the coverage can be fixed for the duration of the policy term (usually 1 to 30 years) or it can be “annually renewable” meaning that the premium can increase each year as you get older. However, the premium for term insurance usually costs less than the premium for permanent insurance when all factors are the same, including the death benefit.

Whole life insurance

Whole life is permanent or cash value insurance that provides insurance coverage for your entire life. With most whole life policies, part of your premium is added to the cash value account, which earns interest. Some whole life policies also pay a dividend, which represents a portion of the company’s profits made during the prior year.

The cash value grows tax deferred and can either be used as collateral to borrow from the insurance company or be directly accessed through a partial or complete surrender of the policy. It is important to note, however, that a policy loan or partial surrender will reduce the policy’s death benefit, there could be income tax implications, and a complete surrender will terminate coverage altogether.

Guarantees are subject to the claims-paying ability and financial strength of the issuing insurance company.

Universal life insurance

Universal life is another type of permanent life insurance with a death benefit and a cash value account. A universal life insurance policy will generally provide very broad premium guidelines (i.e., minimum and maximum premium payments), but within these guidelines you can choose how much and when you pay premiums. You are also free to change the policy’s death benefit directly (again, within the limits set out by the policy) as your financial circumstances change. But if you want to raise the amount of coverage, you’ll need to go through the insurability process again, probably including a new medical exam, and your premiums will increase.

Variable life insurance

Variable life insurance is a type of cash value coverage that allows you to choose how your cash value account is invested. A variable life policy generally contains several investment options, or subaccounts, that are professionally managed to pursue a stated investment objective. Choices can range from a fixed interest subaccount to an international growth subaccount. Variable life insurance policies require a fixed annual premium for the life of the policy and may provide a minimum guaranteed death benefit. If the cash value exceeds a certain amount, the death benefit will increase.

Variable universal life insurance

Variable universal life combines all of the options and flexibility of universal life with the investment choices of a variable policy. You decide how often and how much your premium payments are to be, within policy guidelines. With most variable universal life policies, you can direct how your premium payments are invested among policy subaccounts. But you get no guaranteed minimum cash value or death benefit, and the investment return and principal value of the investment options will fluctuate.

Proceeds from your life insurance can help your spouse pay for services that keep the household running and allow your spouse to keep working.

Joint and survivor life insurance

You and your spouse may choose to buy a single policy of permanent insurance that covers both of your lives. With first-to-die, the death benefit is paid at the death of the spouse who dies first. With second-to-die, no death benefit is paid until both spouses are deceased. Second-to-die policies are commonly used in estate planning to pay estate taxes and other expenses due at the death of the second spouse. Other than the fact that two people are insured by one policy, the policy characteristics remain the same.

Bottom line

Life insurance protection for women is equally as important as it is for men. However, women’s life insurance coverage is often inadequate. It may be time to consult an insurance professional who can help you assess your life insurance needs, and offer information about the various types of policies available.