There has been no shortage of market drama this year, and market uncertainty abounds as we enter 2023.

Through it all, our team at CD Wealth Management continued to send market reminders: This, too, will pass. Focus on the future. Don’t try to time the market. Keep emotions out of market decisions. Stay disciplined.

As with every year, different market themes arose from month to month — and some of those themes occasionally repeated themselves, as history often does.

• After more than 2½ years, COVID continues to play havoc on the global economy. For most of 2022, China continued strict lockdowns and only recently has agreed to ease restrictions after protests from its citizens.

• Russia’s invasion of Ukraine, a war that seems to have no end, brings a tragic loss of lives, an energy crisis in Europe — and maybe the end of Putin’s reign?

• We’re experiencing a bear market. The only thing that goes up is correlations – inflation and higher energy prices, with stocks and bonds both declining.

• Are we in a period of stagflation, deflation or inflation, and what does this all mean?

• The 10-year Treasury note has logged its worst performance in 234 years! The Fed raised rates seven times in 2022, and the Fed funds rate rose from 0 to 4.25%. The entire yield curve is now inverted, with even the 1-month Treasury yielding more than the 10-year Treasury.

• Are we in a recession or not? The Wall Street Journal reports that 90% of investors expect the U.S. to enter a recession before the end of 2023. Everybody seems to agree a recession is coming, but nobody can say for sure.

• The bubble burst on the speculation in the market — crypto, SPACs, NFTs — and high-growth stocks have been decimated as changing risk preferences reined in speculation.

• How have stocks performed since the midterm elections? Historically, a split Congress and White House is the best-case scenario for the markets.

• Tax loss harvesting remains a prudent portfolio management strategy, not just for the end of the year but throughout the year as well — especially in a year like 2022.

Our No. 1 priority is to take care of our clients, and we are proud of the work we have done this year. We wish you a very happy holiday season!

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. CD Wealth Management and Bluespring Wealth Partners LLC* are affiliates of Kestra IS and Kestra AS. Investor Disclosures: https://bit.ly/KF-Disclosures

*Bluespring Wealth Partners, LLC acquires and supports high quality investment adviser and wealth management companies throughout the United States.

Time slows down for no one. It is hard to believe we are already in the fourth quarter of 2022.

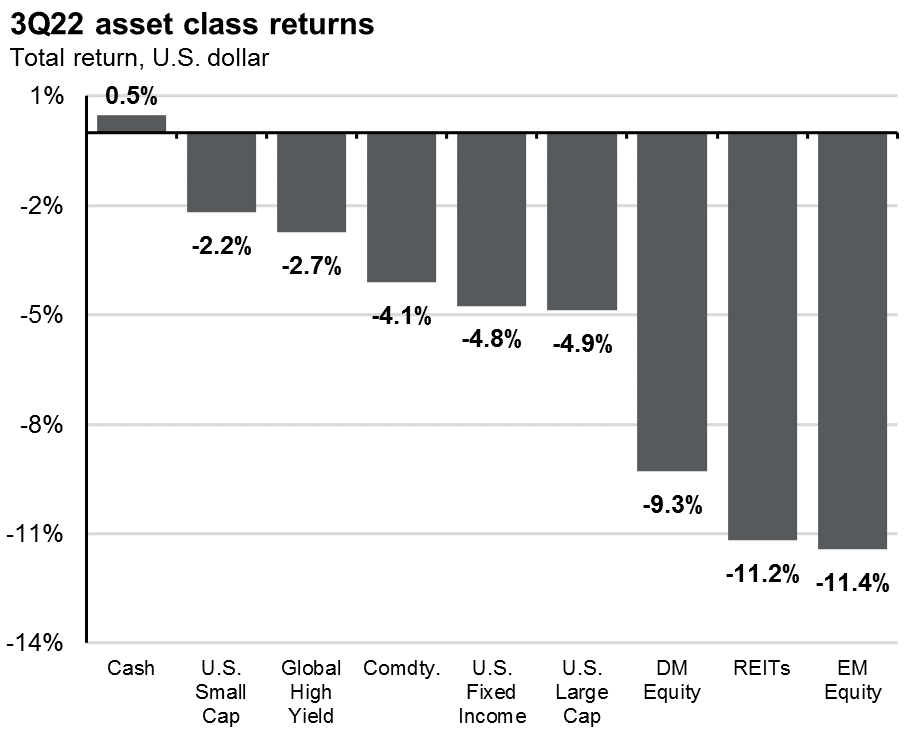

The third quarter of the year saw financial assets continue their decline, as all asset classes — other than cash — delivered negative returns. The Fed’s third consecutive rate hike of 75 basis points (.75%) put further pressure on stocks and bonds. The summer rally we saw in July and early August was erased during the second half of the quarter as inflation continued to rear its ugly head.

The strong correlation of returns between stocks and bonds remained, as bonds were down almost 5% for the quarter. Credit quality in bonds has remained stable this year. However, slower growth, persistent inflation and higher rates could increase credit risk in the coming months. The S&P 500 and NASDAQ both had their worst months since 2008, and the Dow had its worst month since 2002.

International stocks remain challenged by higher energy costs and the ongoing war in Ukraine. Developed markets were down over 9%, and emerging markets were the worst performing in the third quarter, down over 11%. The United Kingdom took strong action last week to step in and purchase bonds to help their markets with additional liquidity.

As we head into the fourth quarter, the main drivers of the market continue to be inflation, China’s path to reopening from the pandemic and war in Ukraine. At the end of the third quarter, we saw a big bounce in short-term interest rates, with the 2-year Treasury trading close to 4.3%. As rates rise, bond prices fall. We are currently seeing high-quality fixed income valuations sitting near 10-year lows.

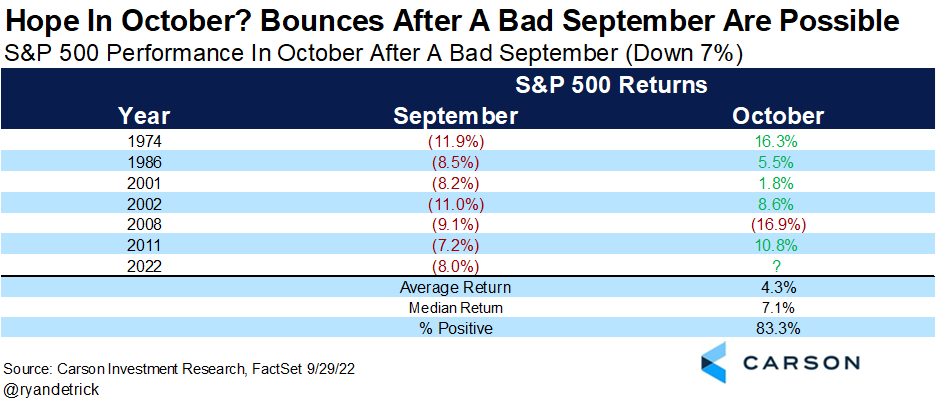

At the same time, S&P 500 forward Price to Earnings (PE) multiples are almost 10% below their long-term averages. These attractive valuations in stocks and bonds historically have led to significant long-term investment opportunities. The chart below shows how the market has responded following a bad month of September — and as we previously wrote, this September was one for the record books. The only instance of a continued slide occurred during the Great Financial Crisis, and we do not believe that this market is similar.

What do we expect for the fourth quarter?

As earnings season starts in a few weeks, most companies are in the process of reducing their earnings forecast based on continued inflationary pressures and higher borrowing costs from rising rates. Only 7% of stocks in the S&P 500 are trading above their 50-day moving average. A month ago, that number was more than 90%. Leading economic indicators continue to show weakness in the global economy, and more economists think a recession may occur in 2023. As we have written many times, the stock market is a leading indicator. By the time the recession arrives, the stock market will be looking ahead and ramping up for the recovery phase.

Here’s what are we watching:

The Federal Reserve: The Fed has forecasted that the Fed Funds rate may move closer to 4.5% by the end of the year. Short-term rates have risen along with the higher Fed Funds Rate. If the Fed indicates it may ease interest rate hikes, we could see a market rally.

International banks: Over the weekend, rumors of potential liquidity issues at Credit Suisse spread through the markets. Questions about risk management and the firm’s ability to compete against larger Wall Street banks sent the stock plunging. Investors fear another “Lehman Brothers moment,” but since the Great Financial Crisis, we have seen a complete overhaul of the banking system to minimize another Lehman scenario.

Market volatility: Market volatility is always unsettling, but historically it is not unusual. We view volatility as an opportunity to purchase more of what you own when we have larger movements in the market.

Midterm elections: As we recently wrote, the S&P 500 has historically outperformed the market in the 12-month period after the election, with an average return of 16.3%. Since 1962, the S&P 500 has not experienced a negative return either six or 12 months following the election. The stock market has historically preferred when one party is in the White House and the other party controls Congress, even if no major legislation is passed.

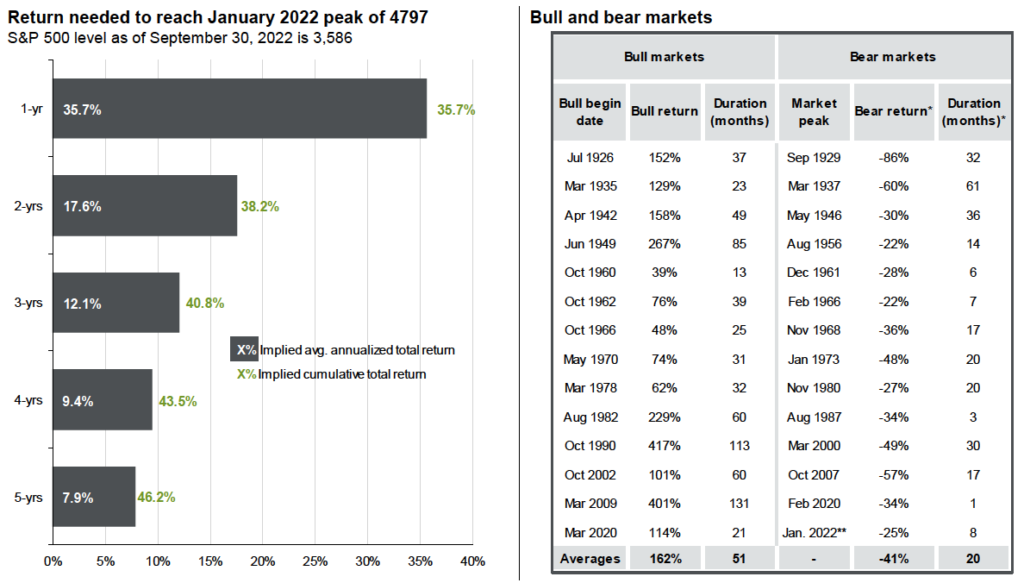

Bear markets do not last forever. We are in a bear market for the Dow, S&P 500 and NASDAQ. Going back to 1929, the average bear market lasts 20 months and has an average loss of 41%, as seen in the chart below on the right. However, the average bull market lasts 51 months and has an average return of 161%. The chart on the left shows how long it may take to get back to the all-time market highs seen in January, depending on the average annual return achieved. Staying invested during these times allows you to participate on the upside when the market recovers – which, historically, it always has.

Equity scenarios: Bull, bear and in between

Source: FactSet, NBER, Robert Shiller, Standard & Poor’s, J.P. Morgan Asset Management. (Left) The current peak of 4797 was observed on January 3, 2022. (Right) *A bear market is defined as a 20% or more decline from the previous market high. The related market return is the peak to trough return over the cycle. Bear and bull returns are price returns. **The bear market beginning in January 2022 is currently ongoing. The “bear return” for this period is from the January 2022 market peak through the current rough. Averages for the bear market return and duration do not include figures from the current cycle. Guide to the Markets — U.S. Data are as of September 30, 2022.

The CD Wealth Formula

We help our clients reach and maintain financial stability by following a specific plan, catered to each client.

Our focus remains on long-term investing with a strategic allocation while maintaining a tactical approach. Our decisions to make changes are calculated and well thought out, looking at where we see the economy is heading. We are not guessing or market timing. We are anticipating and moving to those areas of strength in the economy — and in the stock market.

We will continue to focus on the fact that what really matters right now is time in the market, not out of the market. That means staying the course and continuing to invest, even when the markets dip, to take advantage of potential market upturns. We continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been.

It is important to focus on the long-term goal, not on one specific data point or indicator. Long-term fundamentals are what matter. In markets and moments like these, it is essential to stick to the financial plan. Investing is about following a disciplined process over time.

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. CD Wealth Management and Bluespring Wealth Partners LLC* are affiliates of Kestra IS and Kestra AS. Investor Disclosures: https://bit.ly/KF-Disclosures

*Bluespring Wealth Partners, LLC acquires and supports high quality investment adviser and wealth management companies throughout the United States.

Last week, the Federal Reserve raised the Federal Funds Rate by another 75 basis points (.75%) for the third consecutive meeting. The current range is 3.00% to 3.25%. The Fed expects the Federal Funds Rate to reach 4.50%, implying another 125 basis points (1.25%) of tightening through interest rate hikes. Chairman Jerome Powell hinted that the goal of taming inflation is likely to induce a recession: “Reducing inflation will likely require a sustained period of below-trend economic growth. No one knows whether this process will lead to a recession or, if so, how significant the recession will be.”

At the same time, the Bank of England, Sweden’s central bank, Bank of Canada and European Central Bank have all raised rates by a minimum of 50 basis points (.50%) in the last few weeks. The global outlook is driven by the impact of central bank actions, as well as war in the Ukraine and lockdowns in China.

Powell’s comments pushed stocks sharply lower and sent the U.S. dollar to a 20-year high. (See our previous article: What Does a Stronger U.S. Dollar Mean for You?) Last Friday, stocks closed at their lowest levels since the pandemic in 2020. Stocks have struggled since an unexpectedly hot inflation report in August shocked investors who were looking for price relief. On top of the recent inflation report and the Fed raising rates again, September historically has been the worst month in the stock market, dating back to 1897. Since 1944, only two months have averaged negative returns, with September averaging down .56%, as shown in the chart below.

Theories abound as to why this is the case. It is generally believed that investors come back from summer vacation and want to sell holdings to lock in gains for the year, while others speculate that September marks the beginning of the period when mutual fund companies start to pay distributions, which triggers tax-loss selling. October has seen the largest decline in terms of percentage — think of the crash of 1987 — but historically has been a strong month on average, returning almost 1%.

Source: CFRA BMO

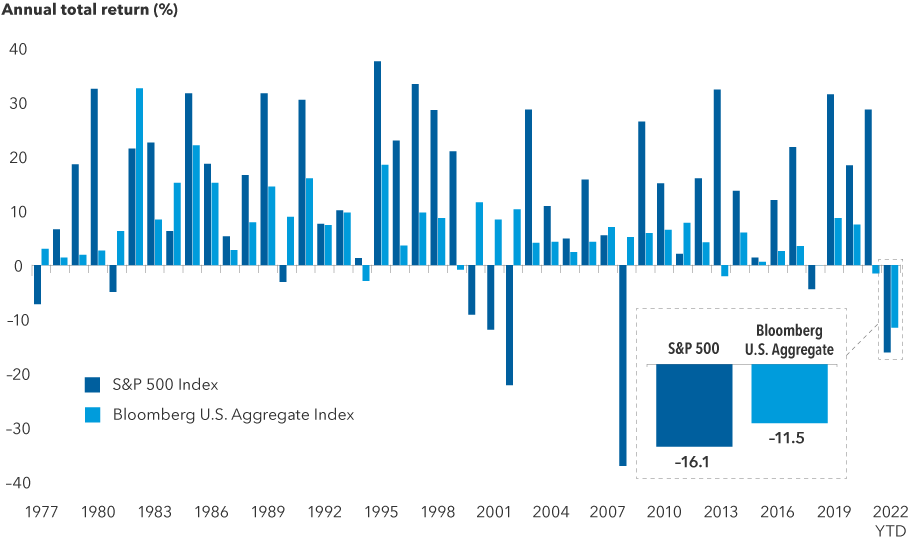

Historically, when stocks have decreased in value, the bond market has been there to offer a “buffer” or help mitigate downside risk. As the chart shows below, in each instance that the S&P 500 has decreased, going back to 1977, bonds have increased. However, that has not been the case this year. Through the end of August, the S&P 500 and the Bloomberg U.S. Aggregate Bond Index are down double digits. Over the last many years, the stock market has been the primary source of returns as money market and bond yields have been close to 0%. These conditions are sometimes called “TINA,” an acronym for “There Is No Alternative.”

We are moving from TINA to TARA — There Are Reasonable Alternatives. With the Fed Funds rate at 3% and the 2-year Treasury bond over 4%, savers can earn more money on their cash alternatives, and investors do not have to reach for excess yield either in the stock market or through lower credit risk in the bond market.

Sources: Capital Group, Bloomberg Index Services Ltd., Standard & Poor’s. Returns above reflect annual total returns for all years except 2022, which reflects the year-to-date total return for both indexes. As of August 31, 2022.

The Fed has made it abundantly clear that it is willing to sacrifice growth for lower inflation. Growth expectations were revised lower for this year and next. The Fed’s new forecast for 2023 Gross Domestic Product (GDP) is 1.2%, with an unemployment rate of 4.4%. The Fed needs both GDP to decline and the unemployment rate to increase for inflation to return to its 2% target level. This is because if the overall output of the economy is increasing, price increases may follow as demand outpaces supply. If GDP is declining, corporate profits are less, and demand is decreasing — which in turn may lead to price decreases.

Much of the most recent inflation increase has been attributed to wage growth. If unemployment increases, then the upward pressure on wages may subside, bringing inflationary pressures down. The economy will be better off the sooner the unemployment rate reaches the “natural rate of employment,” which is the rate that is neither too low and inflationary nor too high and recessionary. At the same time, for the economy to turn the corner, demand and growth need to subside to help with inflationary pressure.

Should inflation begin to recede through a soft labor market and slowing GDP, markets may rebound on prospects for an end to the aggressive rate hikes of 2022. We will need to see several months of evidence that services inflation and wage inflation are trending down. It is critical to remain forward-looking and invested. The fourth quarter is historically the strongest quarter of the year. Missing out on the market rebound, when the largest up days typically occur in a bear market, can be detrimental to the long-term plan that has been constructed for both the good and bad times.

The CD Wealth Formula

We help our clients reach and maintain financial stability by following a specific plan, catered to each client.

Our focus remains on long-term investing with a strategic allocation while maintaining a tactical approach. Our decisions to make changes are calculated and well thought out, looking at where we see the economy is heading. We are not guessing or market timing. We are anticipating and moving to those areas of strength in the economy — and in the stock market.

We will continue to focus on the fact that what really matters right now is time in the market, not out of the market. That means staying the course and continuing to invest, even when the markets dip, to take advantage of potential market upturns. We continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been.

It is important to focus on the long-term goal, not on one specific data point or indicator. Long-term fundamentals are what matter. In markets and moments like these, it is essential to stick to the financial plan. Investing is about following a disciplined process over time.

Sources: American Funds, CFRA BMO, Schwab

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. CD Wealth Management and Bluespring Wealth Partners LLC* are affiliates of Kestra IS and Kestra AS. Investor Disclosures: https://bit.ly/KF-Disclosures

*Bluespring Wealth Partners, LLC acquires and supports high quality investment adviser and wealth management companies throughout the United States.

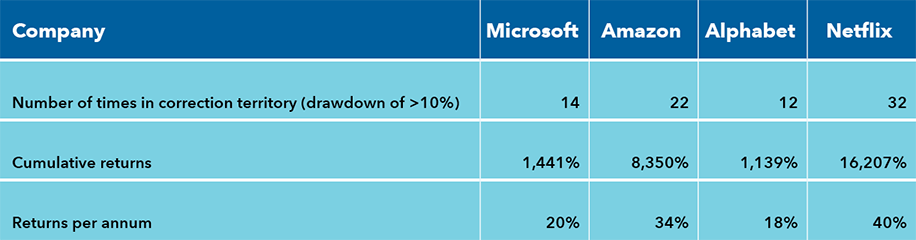

Persistent worries about inflation and tightening monetary policy led to January’s market sell-off and NASDAQ’s worst month since the onset of the pandemic in March 2020. The average stock in the NASDAQ composite has experienced a decline of about 47% from its peak, according to a JP Morgan Report. Renewed geopolitical tensions, ranging from the Russia-Ukraine crisis to U.S.-China relations, also are fueling market volatility. And though market volatility is likely to persist, this does not mean that the stock markets will continue to experience similar downward pressure for the remainder of the year.

Volatility in growth companies is to be expected in any market environment. Over the past 15 years, some well-known, fast-growing companies experienced multiple corrections that were similar to the ones we encountered in January. Those who remained invested and weathered the market turbulence have realized attractive returns over the long term.

Sources: Capital Group, Morningstar Direct. As of Dec. 31, 2021. Corrections defined by share price decline of 10% or greater. Based on daily returns from 2007 to 2021.

Many positives remain for the current economy. GDP, which was reported last week for 2021, grew at an annualized rate of 5.7% — the fastest growth since 1984. Most economists expect the GDP to grow at a much lower rate for 2022 as fiscal stimulus wanes and monetary policy tightens. The first-quarter GDP is expected to be .1% and around 2% to 3% for the year. While this prediction would mean slower growth this year — thanks to economic drag from COVID and supply-chain tightness — it does not mean a recession is likely. By definition, a recession happens when there are two consecutive quarters of negative GDP growth. Based on economists’ predictions that GDP will be positive and growing, we do not see the economy headed into a recession.

As we wrote last week, the market has tended to rise in periods following initial increases in interest rates. The Fed is intent on normalizing interest rates. The current levels of inflation are driven mainly by supply constraints following a huge shift in demand during the pandemic, not by an overheated economy.

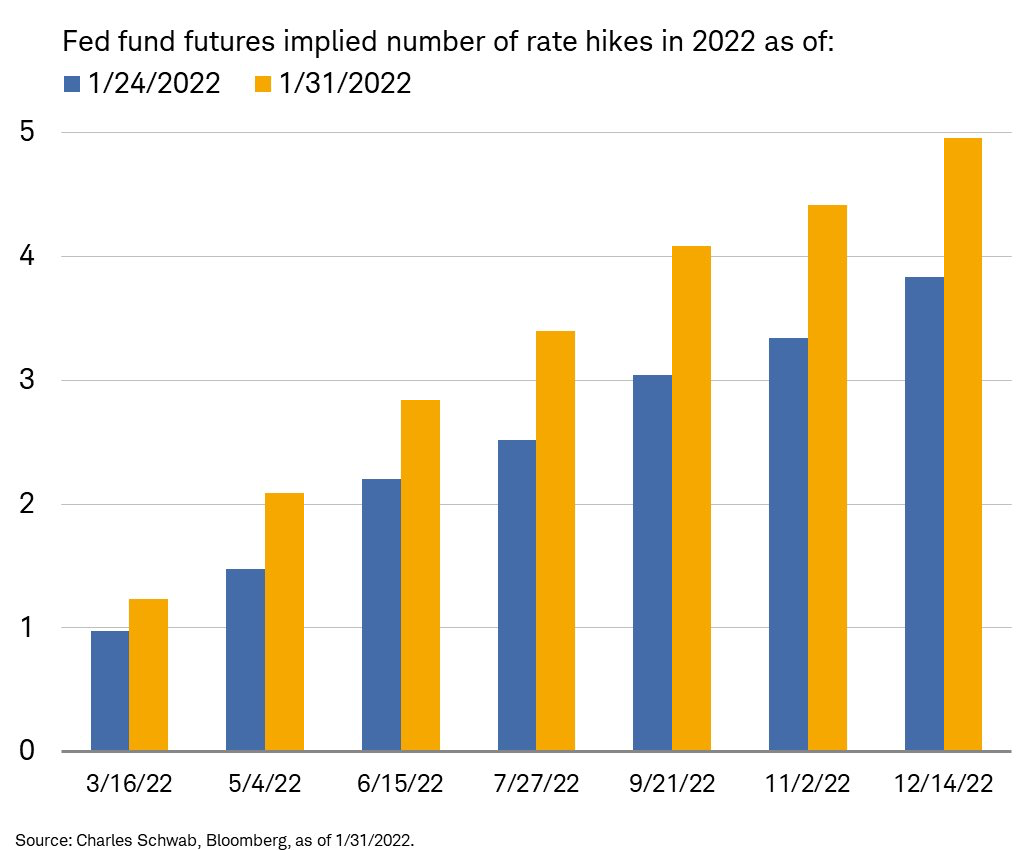

We continue to believe that the path toward monetary policy normalization will be bumpy as the Fed raises rates and tapers bond purchases, and we predict that volatility will continue to exist in the markets. Questions remain as to how many interest rate hikes the Fed will implement in 2022. As the chart below shows, even the change from one week differs on expectations for rate hikes in 2022.

The uncertainty around Fed policy in a highly fluid environment has been the main driver of recent market volatility. Until there is greater clarity from the Fed on inflation, we expect these choppy market conditions to continue.

So, what can we learn from all this? In markets and moments like these, it is essential to stick to the financial plan and not to panic. It’s important to remember that panic is not an investing strategy. Neither are “get in” or “get out” — those sentiments are just gambling on moments in time. Investing is a disciplined process, done over time.

From a portfolio perspective, we continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been. Making market decisions based on what might happen may be detrimental to long-term performance. The key is to stay invested and stick with the financial plan. Markets go up and down over time, and downturns present opportunities to purchase stocks at a lower value. As we say each week, it is important to stay the course and focus on the long-term goal, not on one specific data point or indicator.

It all starts with a solid financial plan for the long run that understands the level of risk that is acceptable for each client. Regarding investments, we believe in diversification and having different asset classes that allow you to stay invested. The best option is to stick with a broadly diversified portfolio that can help you to achieve your own specific financial goals — regardless of market volatility. Long-term fundamentals are what matter.

Sources: American Funds, JP Morgan, Schwab

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. Kestra IS and Kestra AS are not affiliated with CD Wealth Management. Investor Disclosures: https://bit.ly/KF-Disclosures

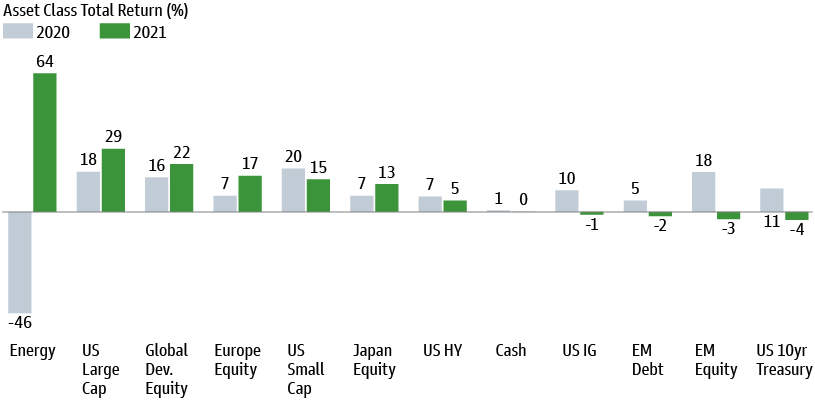

In all, 2021 was a solid year for the financial markets. The economy’s ability to adapt to the pandemic, the vaccine rollout, additional financial stimulus and easy monetary policy all supported strong performance. Growth in large-cap U.S. equities was primarily driven by gains among the S&P 500’s largest tech holdings. Severe supply-chain bottlenecks and a surge in energy prices supported a strong commodity performance. Small-cap U.S. equities trailed their large-cap counterparts but still produced returns greater than their 20-year average of 11%.

Outside the U.S., equities in developed markets had another strong year. Emerging markets, on the other hand, were hurt after a correction in the Chinese stock market and continued lockdown measures. Finally, U.S. fixed income decreased as long-term interest rates ended the year higher than where they started.

The Chinese stock market had a correction in 2021, and questions remain about the Chinese economy. The property market downturn, triggered by the collapse of Evergrande, is a large drag on China’s economic growth. In the past, downside growth risks in China have been quickly countered by monetary and fiscal stimulus. This time may be different as signals point toward Chinese leaders being worried about excessive leverage in the property sector. With China’s 2022 growth projections being around 5%, this may take some pressure off global inflation.

In 2022, the central narrative will be how markets react to the Federal Reserve and other major central banks transitioning away from an extraordinary 18-month period of stimulus. Return and income-seekers will need to navigate a backdrop of favorable but moderating growth, high valuations, low and rising yields, and ongoing COVID-related question marks — in particular, an uncertain path for inflation.

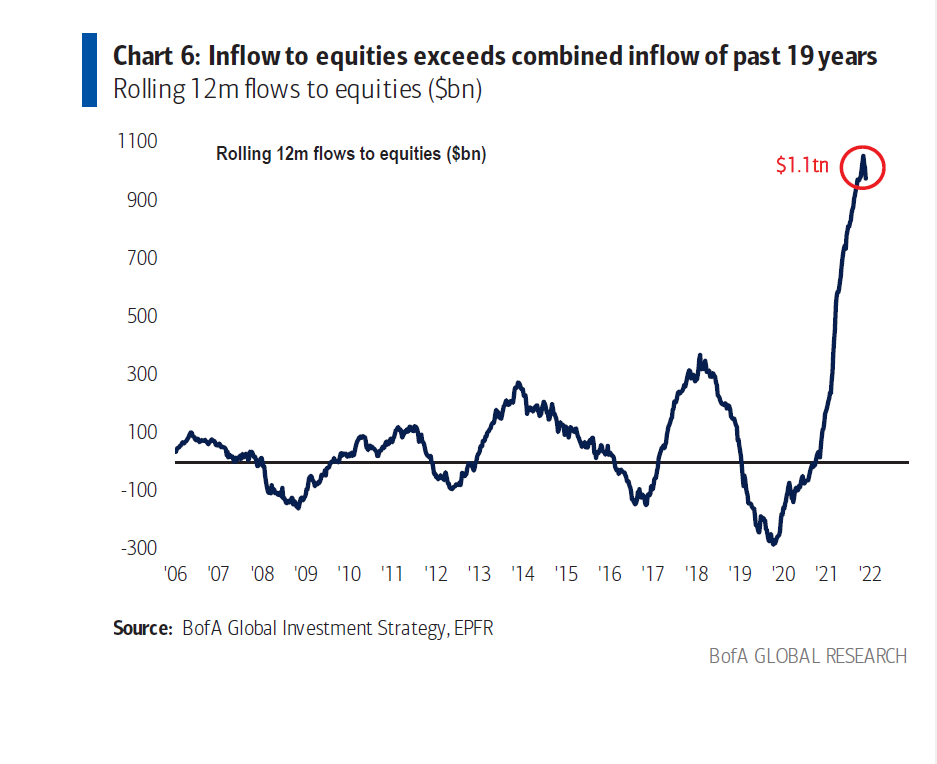

The U.S. economy is poised for a year of moderating but above-trend economic growth. Robust household income and accumulated savings leave the consumer in a strong position heading into the year. Businesses have record levels of cash on hand, which may lead to record levels of investment. Unemployment is at 4.2%, and wages are up. Excess cash has been moving into the equity markets, and in 2021, inflows into equities were more than the past 19 years combined.

Inflation remains the primary focus for most investors. Moderating demand, rebalancing demand from goods to services and healing the supply side should allow inflation to rates to reduce in the second half of the year. Wage inflation and strong labor demand are the key risks to this scenario. At the same time, we are keeping a close watch on fiscal policy. For now, President Biden’s Build Back Better plan is on ice. If this plan were to be resurrected, we would watch closely and keep you informed every step of the way.

So, what can we learn from all this? We are hopeful that 2022 will be a turning point in the global pandemic and that policy makers will wean economies and markets off fiscal and monetary stimulus. Vaccine manufacturing continues to ramp up, and new therapeutics to fight COVID continue to be available in the U.S. and abroad. Inflationary pressures should ease but still settle at an elevated level than the recent past. We believe that diversification and the discipline to stay invested over the long-term are more important than ever. We are optimistic for a successful 2022!

From a portfolio perspective, we continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been. Making market decisions based on what might happen may be detrimental to long-term performance.

The key is to stay invested and stick with the financial plan. Markets go up and down over time, and downturns present opportunities to purchase stocks at a lower value. As we say each week, it is important to stay the course. and focus on the long-term goal, not on one specific data point or indicator.

It all starts with a solid financial plan for the long run that understands the level of risk that is acceptable for each client. Regarding investments, we believe in diversification and having different asset classes that allow you to stay invested. The best option is to stick with a broadly diversified portfolio that can help you to achieve your own specific financial goals — regardless of market volatility. Long-term fundamentals are what matter.

Sources: BofA Global Investment Strategy, Blackrock, Bloomberg, JP Morgan, Russell Investments

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. Kestra IS and Kestra AS are not affiliated with CD Wealth Management. Investor Disclosures: https://bit.ly/KF-Disclosures

We are excited for 2022 and are looking forward to a great year ahead. It’s hard to believe we are nearly two years into the pandemic. It has been a balancing act on a global scale as governments and central banks gauged how much fiscal and monetary stimulus was needed to boost economies without creating runaway inflation.

We see many positives for the financial markets heading into 2022:

1. Global growth continues to be positive. 2. Monetary and fiscal policy are still supportive of growth, even in the face of tapering and possible interest rate hikes in 2022. 3. Congress recently passed legislation to raise the debt ceiling for all of 2022. 4. There is potential for peak inflation and lower inflation for the second half of 2022. 5. The easing of supply chain issues should help both emerging and developed international markets. 6. Consumer spending is strong, and balance sheet savings rates are higher.

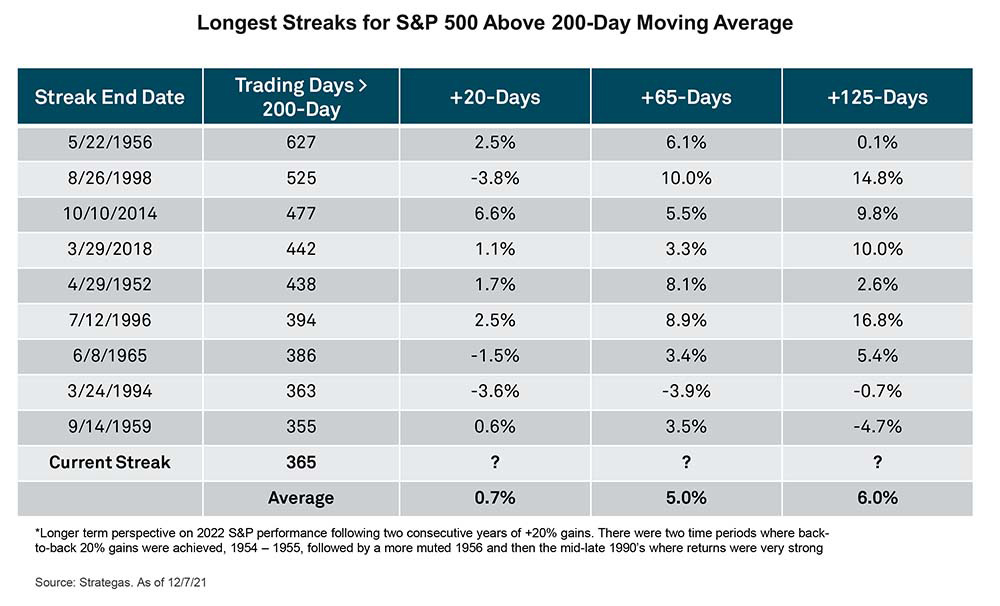

The S&P 500 has traded above the 200-day moving average for all of 2021. The chart below suggests that when the S&P 500 is above its 200-day moving average, forward returns are often favorable.

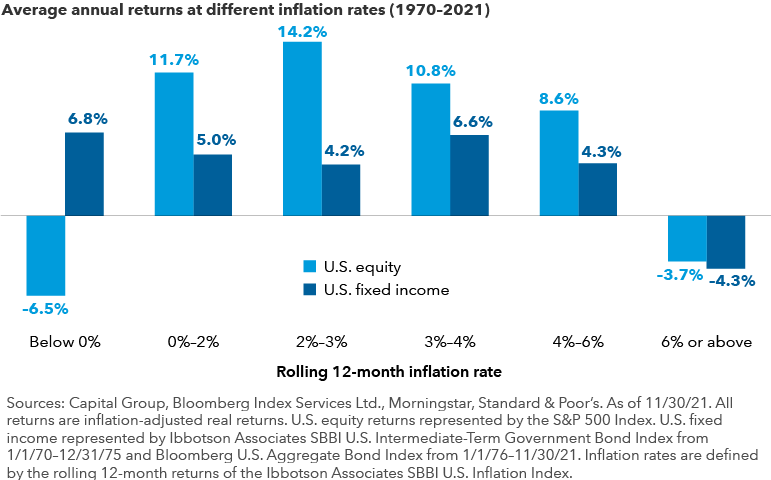

Clearly, inflation and its effect on the stock market are on the top of everyone’s mind. Remember that some inflation can be healthy for companies because it allows them to raise prices and increase profitability. Also, as seen in the chart below, stocks and bonds have generally provided solid returns, even during times of higher inflation. It is during the extremes that the markets often tend to struggle, but as inflation moderates, stocks and bonds can have strong years.

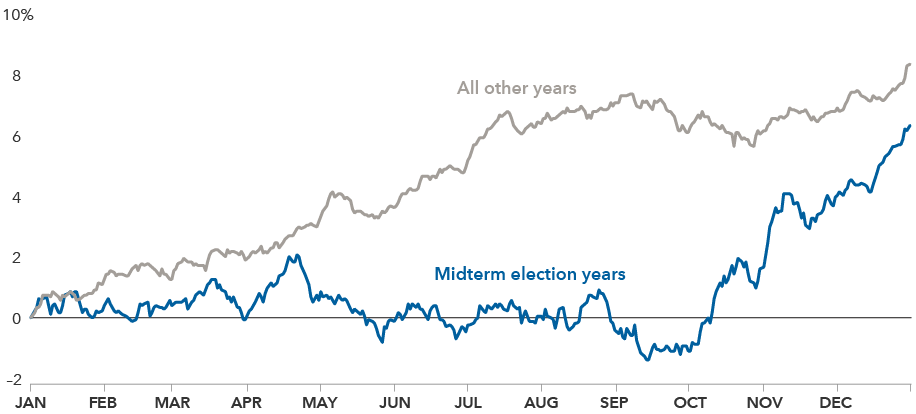

Political uncertainty often has a noticeable short-term effect on the markets. An analysis of more than 90 years of equity returns reveals that stocks tend to have lower average returns and higher volatility for the first several months of midterm election years. The trend often reverses, and markets have tended to return to their normal trajectory. Remember, the numbers below are just averages; it is important not to try to time the market. Elections generally create a lot of noise, so it is important to look past the short-term highs and lows and focus on the long-term picture instead.

S&P 500 Index average returns since 1931

The markets and the global economy are not without risks. History shows us that the biggest risks in a typical year are hiding in plain sight, not suddenly appearing out of nowhere. Risk appears when there is a high degree of confidence among market participants expecting a specific outcome that doesn’t pan out. If we look to identify the unexpected, we see the following as potential risks to the global markets in 2022:

1. Supply chain shortages turn into gluts: Whether it’s semiconductors, used cars or a variety of products, any potential supply glut in 2022 may lead to a fall in inflation. Excess inventory would promote price cuts and pose risks to industries that have thrived on pricing boosts from shortages. 2. Rate hikes slower than expected: Surging inflation has led the Fed to anticipate three rate hikes in 2022. If inflation eases, the expectations for the number of rate hikes may change as well. 3. China: The World Bank cut its forecasts for China’s economy in 2022 after the nation’s continued attempts to restrict business, break up large technology companies and remove bitcoin mining. 4. COVID outbreaks and new strains: Investors may have grown confident in trading rotation in and out of stocks depending on the seasonality and COVID flare-ups. If the current and future waves have less impact on the overall economy, the stocks that have led us out of the economic doldrums may not have the same effect going forward. 5. Geopolitical surprises: The biggest worry could be a military conflict, whether that is China and Taiwan, an invasion of Ukraine by Russia or even a regional conflict in the Middle East.

History doesn’t always repeat itself, but similarities often exist. While inflation on a year-over-year basis is high, this is not the runaway inflation of the 1970s. Today’s inflation is more akin to the 1920s and 1950s, when we witnessed booms in productivity and innovation and the rebuilding of an economy boosted by a new generation of household spending, along with new infrastructure spending. The markets may experience elevated volatility in the coming year as the above risks test the markets. We will continue to keep you informed and invested through the ups and downs of 2022.

So, what can we learn from all this? We are hopeful that 2022 will be a turning point in the global pandemic and that policymakers will wean economies and markets off fiscal and monetary stimulus. Vaccine manufacturing continues to ramp up, and new therapeutics to fight COVID continue to be available in the U.S. and abroad. Inflationary pressures should ease but still settle at a level higher than the recent past. We believe that diversification and the discipline to stay invested over the long term are more important than ever. We are optimistic for a successful 2022!

From a portfolio perspective, we continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been. Making market decisions based on what might happen may be detrimental to long-term performance. The key is to stay invested and stick with the financial plan. Markets go up and down over time, and downturns present opportunities to purchase stocks at a lower value. As we say each week, it is important to stay the course, focusing on the long-term goal and not on one specific data point or indicator.

It all starts with a solid financial plan for the long run that understands the level of risk that is acceptable for each client. Regarding investments, we believe in diversification and having different asset classes that allow you to stay invested. The best option is to stick with a broadly diversified portfolio that can help you to achieve your own specific financial goals — regardless of market volatility. Long-term fundamentals are what matter.

Sources: Capital Group, Charles Schwab, BNY Mellon

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. Kestra IS and Kestra AS are not affiliated with CD Wealth Management. Investor Disclosures: https://bit.ly/KF-Disclosures

As 2021 comes to an end, let’s reflect on the rollercoaster ride we took together.

In January, while we were still in the midst of the global pandemic, we witnessed an insurrection at the Capitol. Thankfully, our government was able to usher in a smooth presidential transition and we quickly returned to business as usual.

Throughout the year, different market themes arose — and some repeated themselves often. Some of the trends and headlines seemed transformational, but in hindsight, the market continued marching on — so much so that you may not even remember some of the issues that captured our attention.

• Special-purpose acquisition companies — better known as SPACs — became one of Wall Street’s hottest trends, accounting for more than two-thirds of Nasdaq’s initial public offerings in January.

• COVID continues to weigh heavily on the minds of investors, from the availability and adoption of vaccinations and boosters to the emergence of variants.

So, what can we learn from all this? COVID is still taking a terrible toll on the U.S. and the world. Even with the new Omicron variant, the U.S. economy looks solid and supply-chain bottlenecks may be easing. We think investors need to be ready to ride the COVID rollercoaster for years to come.

Panic is not a strategy when dips occur. When the market falls and volatility rises, the plan is to stay the course and consider those opportunities as buying chances, not as a time to panic and sell.

We gladly welcomed clients back to our office in 2021, and we look forward to seeing you again in our office in 2022. We continue to stay connected with you through Zoom or in person. Our team continues to have our daily internal meetings every morning and night via Zoom to ensure we stay connected and work together.

Our No. 1 priority is to take care of you, our clients, and we are proud of the work we have done this year. We are grateful for you!

————

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. Kestra IS and Kestra AS are not affiliated with CD Wealth Management. Investor Disclosures: https://bit.ly/KF-Disclosures

Last week, the stock market pulled back in a very volatile week as investors grappled with the potential impact of the Omicron COVID variant and commentary from Fed Chair Jerome Powell that the risk of inflation has increased. Powell also said the Fed may consider speeding up its bond purchase tapering plans and hinted at potential earlier rate hikes in 2022.

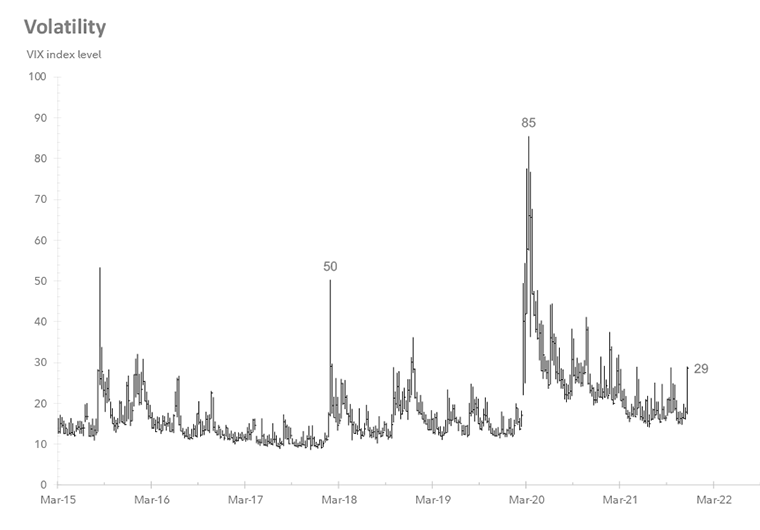

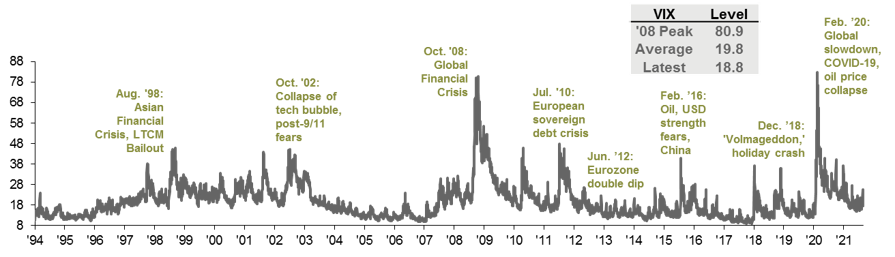

As a refresher, the VIX index is a measure of forward-looking stock market volatility for the next 30 days. The VIX is known as the fear gauge; it reflects the market’s short-term outlook for stock price volatility as derived from option prices on the S&P 500. On Monday, the VIX topped out at 35, after having traded at below 20 for most of October and November — that’s a 75% increase in the volatility index in a very short period. As the chart below shows, we have had many short-lived, volatile market movements over the past 20 months. In hindsight, the spikes in volatility have allowed investors to continue to “buy the dip” in the accompanying market sell-offs. As volatility then wanes, the market recovers.

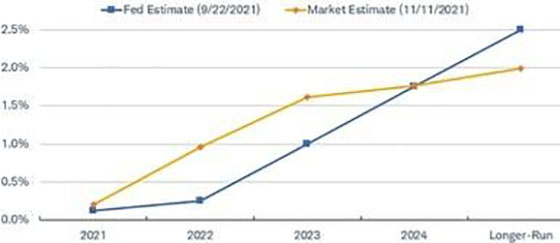

One of the primary causes of the recent increase in volatility is inflation. The Fed belatedly acknowledged inflation risks, and we expect it to start raising rates next year. What matters is not that they are going to raise rates, but the rate trajectory and where they end up next year and going forward. The chart below shows the Fed estimate as well as the market estimate for interest rates. Both the market and the Fed predict that short-term rates will be around 1.75% in 2024, which would be a slow, steady increase from where they are now: 0-0.25%.

The Fed’s view of the path of rate hikes vs. the market’s view

Note: The 12/15/2027 eurodollar futures rate was used for the Longer-Run market rate. Source: Bloomberg. Fed estimate as of 9/22/2021. The market estimate of the federal funds rate using eurodollar futures (EDSF). As of 11/10/2021.

Also weighing on the markets and causing increased volatility is the work Congress still has to do before the end of the year, with several large issues to resolve:

* Defense spending bill: Congress is near agreement to authorize $770 billion in military spending.

* Keeping government open: President Biden signed a stopgap spending bill that will keep the Federal Government running through Feb. 18.

* Social spending bill: The Build Back Better Plan could also drag into next year as negotiations on how to fund the bill continue.

* Raising the debt ceiling: The estimated deadline is Dec. 15. Raising the debt ceiling does not allocate new spending; it only authorizes the Treasury to make good on current obligations.

This year’s series of events has no historical parallel: a growth surge from a global pandemic, a supply-driven spike in inflation and a change in Federal Reserve monetary policy that is being tested in real time.

The COVID shock was more like a natural disaster than the economic restart from a global financial crisis. Economic activity surged, and corporate profits rebounded at a rapid pace.

Demand for goods — rather than services — along with supply-chain bottlenecks have driven prices higher. We expect that prices eventually will be higher than pre-COVID levels, but supply and demand ultimately will determine where they settle. As supply-chain bottlenecks open and more goods are available to the public, prices will come down as demand decreases. At the same time, the service industry also will begin to see increased demand, which may reduce the demand for goods, in turn reducing prices as well.

So, what can we learn from all this? COVID is still taking a terrible toll on the U.S. and the world. Even with the new Omicron variant, the U.S. economy looks solid and supply-chain bottlenecks may be easing. We think investors need to be ready to ride the COVID rollercoaster for years to come. Panic is not a strategy when dips occur. When the market falls and volatility rises, the plan is to stay the course and consider those opportunities as buying chances, not as a time to panic and sell.

From a portfolio perspective, we continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been. Making market decisions based on what might happen may be detrimental to long-term performance. The key is to stay invested and stick with the financial plan. Markets go up and down over time, and downturns present opportunities to purchase stocks at a lower value. As we say each week, it is important to stay the course and focus on the long-term goal, not on one specific data point or indicator.

It all starts with a solid financial plan for the long run that understands the level of risk that is acceptable for each client. Regarding investments, we believe in diversification and having different asset classes that allow you to stay invested. The best option is to stick with a broadly diversified portfolio that can help you to achieve your own specific financial goals — regardless of market volatility. Long-term fundamentals are what matter.

Sources: Bloomberg, Blackstone, Fidelity

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. Kestra IS and Kestra AS are not affiliated with CD Wealth Management. Investor Disclosures: https://bit.ly/KF-Disclosures

Last Friday, news of a COVID-19 variant identified in South Africa and new travel restrictions sent markets tumbling and injected volatility into the markets. The Dow Jones Index slid 900 points to suffer its worst day since October 2020. The news was exacerbated in the stock markets, as the Friday after Thanksgiving is typically a low-volume trading day and a shorter trading day due to the holiday. Oil prices fell more than 12% in one day, with news of potential lockdowns across the globe, though President Biden reiterated that the U.S. will not initiate economic lockdowns or new travel restrictions.

The market has continued its sell-off this week as Moderna and Regeneron separately commented on the effectiveness of the current vaccines against the new variant. At the same time, Fed Chairman Jerome Powell told the Senate that he expects tapering could wrap up a few months sooner than anticipated and that it is time to stop describing inflation as “transitory,” opening the possibility for the Fed to raise rates in early 2022.

The chart below reflects the overall market returns through Nov. 26. While the markets have had a strong year, most underlying holdings are trading in a correction mode. This further supports that the underlying market may not be as expensive as many people fear.

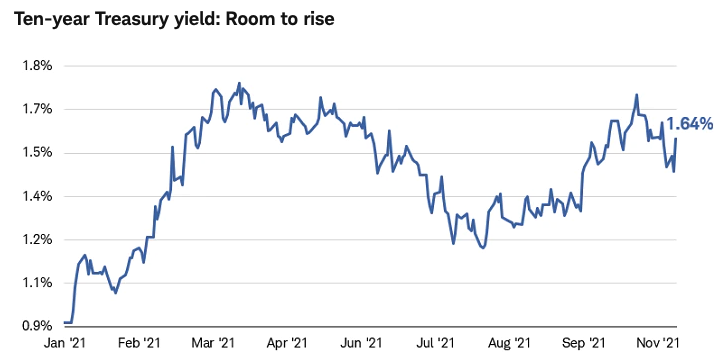

It hasn’t been the smoothest of sailing for fixed income investors in 2021. Bond yields have ridden waves of optimism and pessimism about the economic outlook for most of the year. The chart below reflects the year’s big swings in the 10-year Treasury. As we near the end of the year, short-term yields have moved up in anticipation of tightening monetary policy — while the 10-year Treasury has fallen back from the levels seen in October, despite inflation.

With more discussion of inflation — and more economists predicting that rates will rise next year — we recently made a portfolio reallocation within our fixed income portion of the portfolio:

1. We are shortening the duration of the fixed income portion of the portfolio. As a refresher, duration is a measure of how long it takes for a bond to repay the principal using both income and principal. In an environment of rising interest rates, we are hopeful that a shorter duration will protect against falling principal compared to longer-duration bonds.

2. We are maintaining similar credit quality within fixed income but adding a short-duration position to hedge against rising rates. We removed our longer-duration investment grade corporate bond position.

3. We also increased the weighting in our strategic income holding to produce additional income in a low interest rate environment.

Our focus remains on long-term investing with a strategic allocation while maintaining a tactical approach. Our decisions to make changes are calculated and well thought-out, looking at where we see the economy and rates heading.

We are not guessing or market timing. We are anticipating and moving to those areas of strength in the economy. We strategically have new cash on the sidelines and buy in for those clients on down days or dips in the market, as one does in a 401(k) every other week. We speak with our clients regularly about staying the course, not listening to the economic noise and trading memo stocks.

So, what can we learn from all this? Hoping that an outcome will or will not occur is not a strategy. In light of new COVID variants, we think investors need to continue to be ready to ride the rollercoaster for years to come. With the most recent quarter’s record earnings, the overall valuation of the market has come down. That does not mean we won’t experience dips and corrections, but when they happen, the plan is to stay the course and consider those opportunities as buying chances — not a time to panic and sell.

From a portfolio perspective, we continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been. Making market decisions based on what might happen may be detrimental to long-term performance. The key is to stay invested and stick with the financial plan. Markets go up and down over time, and downturns present opportunities to purchase stocks at a lower value. As we say each week, it is important to stay the course and focus on the long-term goal, not on one specific data point or indicator.

It all starts with a solid financial plan for the long run that understands the level of risk that is acceptable for each client. Regarding investments, we believe in diversification and in having different asset classes that allow you to stay invested. The best option is to stick with a broadly diversified portfolio that can help you to achieve your own specific financial goals — regardless of market volatility. Long-term fundamentals are what matter.

Sources: CNBC, Schwab

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. Kestra IS and Kestra AS are not affiliated with CD Wealth Management. Investor Disclosures: https://bit.ly/KF-Disclosures

September held true to its history of being the worst month for performance on average since the S&P 500’s inception in 1928. The month ended with increased volatility (as measured by the VIX index) and negative market sentiment. Its negative market returns marked the first time in eight months that the S&P 500 ended a month in negative territory. There was no shortage of risks working against the financial markets, including debt ceiling negotiations, fiscal policy uncertainty, monetary policy uncertainty, global supply chain bottlenecks, slowing economic growth projections from the Delta variant and ongoing inflation fears.

The chart below depicts the VIX index over the last 27 years. Volatility has risen recently, reflecting the possibility of a broader distribution of potential market outcomes based on many of the risks listed above. We are a far cry from volatility levels seen during the financial crisis of 2008 or the global pandemic in 2020, however; the VIX index remains below average heading into the fourth quarter of the year.

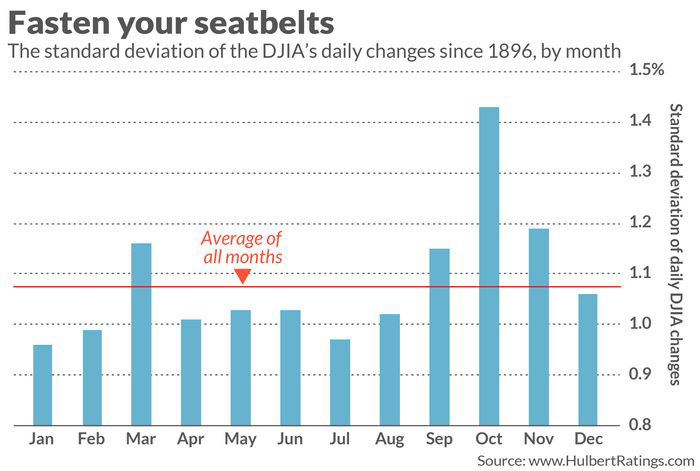

October remains the most volatile month of the calendar, as you can see from the chart below. October’s above-average volatility isn’t a function of any one year or a presidential cycle; it has been consistent over decades and market cycles. As volatility increases, it doesn’t necessarily mean that the market will go down more — but it does mean that the ranges of market movements increase. Often, with increased volatility comes increased emotion accompanying the ups and downs. The feeling of panic when the market is moving down feels greater than the relief or joy feels when the market is moving up.

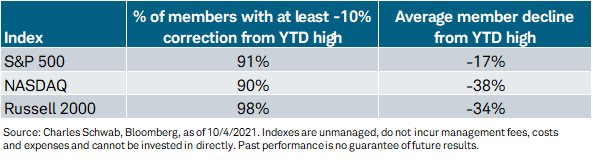

As we wrote last week, more than 90% of the S&P 500 holdings have had at least a 10% correction from their highs this year. The same now holds true for both the NASDAQ and Russell 2000 (small cap stock index). Looking further under the hood of each index below, the average stock decline is far greater than the 10% correction.

So, what can we learn from all this? With many stocks already in correction mode and potential increased volatility on the horizon, it is important to remember that investing is a disciplined process and not a game of timing when to get in or when to get out of the market. “Buy the dip” continues to be a prominent strategy among many investors and one of the reasons market pullbacks have not been as prominent in 2021. The larger dips we have seen recently as volatility has increased have led to some larger declines, followed by stronger bounce backs. As we say each week, it is important to stay the course and focus on the long-term goal — not on one specific data point or indicator.

From a portfolio perspective, we continue to adhere to the tried-and-true disciplines of diversification, periodic rebalancing and looking forward, while not making investment decisions based on where we have been. Making market decisions based on what might happen may be detrimental to long-term performance. The key is to stay invested and stick with the financial plan. Markets go up and down over time, and downturns present opportunities to purchase stocks at a lower value.

It all starts with a solid financial plan for the long run that understands the level of risk that is acceptable for each client. Regarding investments, we believe in diversification and having different asset classes that allow you to stay invested. The best option is to stick with a broadly diversified portfolio that can help you to achieve your own specific financial goals — regardless of market volatility. Long-term fundamentals are what matter.

Sources: JP Morgan, MarketWatch, Schwab

This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

Using diversification as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

Past performance is not a guarantee of future results.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation.

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (Kestra AS) an affiliate of Kestra IS. Kestra IS and Kestra AS are not affiliated with CD Wealth Management. Investor Disclosures: https://bit.ly/KF-Disclosures